Authored by Patrick Watson via MauldinEconomics.com,

Here’s a loaded question for you: “What could go wrong?”

In some contexts, it can express mistaken confidence, as in, “Sure I’ll put my hand between that crocodile’s jaws. What could go wrong?”

Investors should ask the same question before entering a position. “What risks am I taking with this trade? What could go wrong if it doesn’t go as planned?”

But here’s the problem: What if you never think to ask the question because you have no idea you’re in that trade?

And guess what—this is your problem if you are a taxpayer anywhere in the US.

Photo: DWS via Flickr

It is my sincere desire to provide readers of this site with the best unbiased information available, and a forum where it can be discussed openly, as our Founders intended. But it is not easy nor inexpensive to do so, especially when those who wish to prevent us from making the truth known, attack us without mercy on all fronts on a daily basis. So each time you visit the site, I would ask that you consider the value that you receive and have received from The Burning Platform and the community of which you are a vital part. I can't do it all alone, and I need your help and support to keep it alive. Please consider contributing an amount commensurate to the value that you receive from this site and community, or even by becoming a sustaining supporter through periodic contributions. [Burning Platform LLC - PO Box 1520 Kulpsville, PA 19443] or Paypal

-----------------------------------------------------

To donate via Stripe, click here.

-----------------------------------------------------

Use promo code ILMF2, and save up to 66% on all MyPillow purchases. (The Burning Platform benefits when you use this promo code.)

Pension Pain

Part of my job is helping John Mauldin with the research for his Thoughts from the Frontline letters. Regular readers know John isn’t a doom-and-gloom guru. He’s optimistic on most of our big challenges.

Except for a few things—like the brewing state and local pension crisis.

The more John and I dig into it, the worse it looks. We have both spent many hours trying to find any good news or a silver lining, without success.

All over the US, states, cities, school districts, and other governmental entities have promised their workers generous retirement benefits, but haven’t set aside enough cash to pay what they will owe. At some point, perhaps soon, either they will have to cut benefits to retirees or stick taxpayers with a huge bill, or both.

You can read John’s September 16 letter, Pension Storm Warning, to learn more. Then you’ll see why he says to Build Your Economic Storm Shelter Now.

What else could go wrong? Plenty.

Photo via Flickr

Healthcare Goes on the Books

Local governments often give retired police officers, firefighters, teachers, and other workers a pension plus healthcare benefits.

Healthcare is expensive even in the best circumstances. Imagine your health insurer had promised to cover your medical expenses but hadn’t set aside any cash to pay for it.

Remarkably, that’s exactly what has happened. Governments currently disclose their retiree healthcare liabilities only in footnotes to their financial statements. Many have saved little to no money to cover those future expenses.

That’s about to change.

Starting in 2018, the Governmental Accounting Standards Board—the source of generally accepted accounting principles (GAAP) for state and local governments—will force officials to record healthcare liabilities on their balance sheets. Pew Charitable Trusts estimates the national shortfall will add up to $645 billion.

That’s on top of the estimated $1.1 trillion in unfunded pension liabilities they already had. In other words, this giant problem that no one knows how to solve is about to get 59% worse!

Or, more accurately, it’s going to look 59% worse. The healthcare shortfall isn’t new. What’s new is that local governments have to stop obscuring it.

What else could go wrong? Plenty.

Photo: AP

Unbudgeted Crisis

Now, let’s add another crisis on top of the already-terrible one that just got 59% worse.

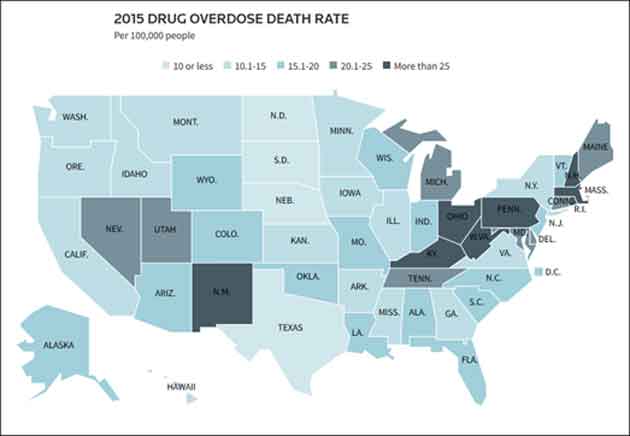

You’ve probably heard about the opioid drug abuse that is killing thousands of Americans. Putting numbers on it is tricky—often, multiple factors contribute to the same death. The Centers for Disease Control estimates opioids played a role in more than 33,000 deaths in 2015. No one thinks the numbers have improved since then.

The deaths aren’t evenly distributed. This Reuters graphic shows the heaviest concentrations in the Midwest, New England, and New Mexico.

It’s probably no coincidence that some of these states also suffered above-average economic pain in the last decade or two.

The deaths from overdose and the even larger number of near-deaths are putting a huge strain on local government finances in those regions.

A recent Reuters investigation found costs soaring for everything from ambulances to autopsies. Cities and counties are racking up huge bills for courts, prosecutors and public defenders, jails, and treatment programs.

The small towns and counties dealing with this opioid plague are often the same ones whose pension plans and healthcare expenses are already underfunded.

That’s bad news for current retirees, workers who hope to retire, and taxpayers who will ultimately foot the bill. In a word, everyone.

But that’s not all.

Costly Storms

Last weekend at the Texas Tribune Festival here in Austin, I heard Houston Police Chief Art Acevedo discuss his Hurricane Harvey experience. As more areas flooded, he kept the entire department on duty for six straight days, 24 hours a day.

Acevedo said he knew this wasn’t in the budget, but the alternatives were worse. Lives were at stake, and the city needed its protectors more than ever.

The hurricane is over, but the Harvey expenses are just starting. Houston may have to spend $250 million on the disposal of flood debris… and the city is only part of the affected area.

Houston’s pension plans were already on shaky ground, so this won’t help. Many local governments in Florida, Puerto Rico, and the US Virgin Islands may see the same, thanks to Irma and Maria.

So what does it mean to you?

For one, we should plan for substantially higher state and local taxes in the future.

And if you’re a public worker or retiree, you better think about how you will make ends meet if your benefits get slashed.

I’m going to do my part by working even harder to find income-generating investments for Yield Shark subscribers, so they can replace what the pension crisis may cost them.

This is, as John Mauldin says, a problem we can’t just muddle through. All we can do is prepare for it—and now is the time to start.

See you at the top,

THE IRS = THEIRS

“And if you’re a public worker or retiree, you better think about how you will make ends meet if your benefits get slashed.”

‘if your benefits get slashed.’

Not if, WHEN. maff ain’t hard at all, dimwits.

This is amongst the reasons why, without my realizing it, my town went from a 9.5% sales tax rate to 10.6%, which only became apparent when I bought a car and paid hundreds more than expected. New shiny buildings for the bureaucrats and police, over-budget revamp of downtown, purchasing land for parks, and… over-large pensions and benefits!

Barring some unforeseen and incredible economic developments, I see no way pensions are going to be paid with dollars anywhere near equal in value to our dollars today the way most people seem to be counting on.

10 years from now you may still get your full pension payments, they just won’t be buying very much.

If we’re still here as a nation in 10 years anyway.

If it CANNOT be fixed then it WON’T be fixed. Lying to yourself will not solve any of these pension problems.

Someone(s) WANT a collapse. How else do you explain ZIRP? It simultaneously punishes every saver, every pensioner and every insurance company in the country. Not that many investments these days can support a decent interest coupon – not when the freaking FED thinks 2% inflation is DESIRABLE!

The nation is run by (a) morons (b) ignorant and rapacious thieves (c) elites who think they can have it all, without consequences. No matter which you choose, the failures are baked in the cake!

Most government pension plans have no where to go but the taxpayers who are already tapped out . Don’t despair government employees your reps have already started the wheels turning . The powers that be are calling all private sector savings and property as “UNTAPPED RESOURCES” ! This means the gang of badged “JUST DOING MY JOB ENFORCERS” will be confiscating , fining and asset forfeiture against average citizens till they are broken and in the street but they will be closer to solvency !

This will be ugly and may get bloody . I am losing my optimism minute by minute

It will be a seriously cold day in hell before I worry about some GEMP (government employee) getting their retirement. It would suit me just fine if all of them were forced to live on Social Security. In fact it would make me one happy Zombie to watch the worthless bastards starve to death while their families were being hacked, raped, and disemboweled. How many times has anyone ever heard one, just one GEMP say, “Gee, I don’t know how I’m going to pay my bills this month?” Huh, anyone. Didn’t think so! Ever heard them say, “I’m so depressed, because I can’t pay my kids tuition this semester.” Nope, again huh. Ever seen one driving a clunker down the highway, wearing shabby clothes, walking behind a push mower, wipe the sweat from their brows, or last but certainly not least, apologize for taxing us into the poor house so they could live the good life. Nope again. Recently a GEMP with the feds retired in my neighborhood at the tender age of 52. He had just bought his 16 year old a brand spanking new $50,000 pickup, cash of course, and then dropped by the local boat dealership to purchase a new bass boat at the cool price of another $30,000 just to celebrate his retirement. Ever see anyone on Social Security do that? Didn’t think so. thanks