Guest post by John P. Hussman

“Stock prices have reached what looks like a permanently high plateau.”

Irving Fisher, October 21, 1929

“Stability leads to instability. The more stable things become and the longer things are stable, the more unstable they will be when the crisis hits.”

Hyman Minsky

“Participants in the speculative situation are programmed for sudden efforts at escape. Thus the rule, supported by the experience of centuries: the speculative episode always ends not with a whimper but with a bang. There will be occasion to see the operation of this rule frequently repeated.”

John Kenneth Galbraith

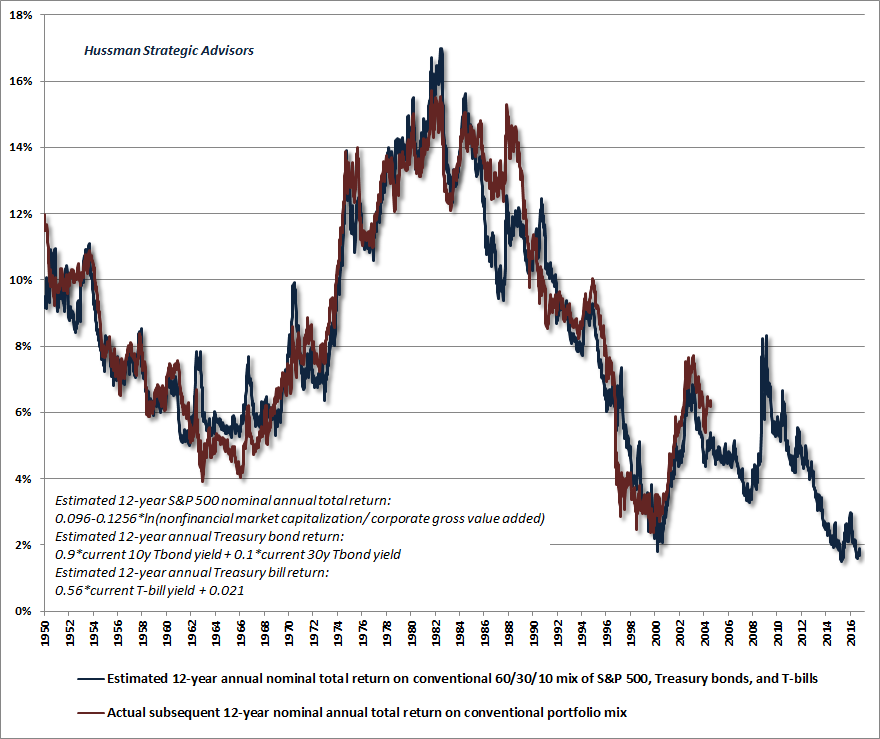

Despite a near-term outlook that remains rather neutral (though with negative skew), we believe that one requires either a disregard or an ignorance of market history to dismiss the likelihood of a 40-55% market retreat over the completion of the current market cycle. From present valuations, a market loss of that magnitude would not be a worst-case scenario, but merely a run-of-the-mill completion of the current market cycle. On a longer horizon, we presently estimate that S&P 500 nominal total returns are likely to average just 0-2% annually over the coming 10-12 years, with negative expected real returns on both horizons. Since the dividend yield on the S&P 500 exceeds 2% here, that also implies that we fully expect the S&P 500 Index to trade at a lower level in 10-12 years than it does today.

The good news here is that in order to achieve a zero 10-12 year return despite deep interim losses, we should also expect opportunities for strong market advances over this horizon. As I’ve noted frequently over the years, the most favorable market return/risk profile we identify is associated with a material retreat in market valuations that is then joined by an early improvement in our measures of market action. I have every expectation that this opportunity will emerge over the completion of the current market cycle.

Based on valuation measures having the strongest correlation with actual subsequent market returns across history, equity valuations have approached present levels in only a handful of instances: 1901 (followed by a -46% market retreat over the following 3-year period), 1906 (followed by a -45% retreat over the following year), 1929 (followed by a -89% collapse over the following 3 years), 1937 (followed by a -48% loss over the following year), 2000 (followed by a -49% market loss over the following 2 years), and 2007 (followed by a -57% market loss over the following 2 years). A few lesser extremes occurred in the 1960’s and 1970’s, followed by market losses in the -35% to -48% range.

Read Hussman’s Weekly Letter