Having infamously spotted and profited from bubbles in Japan in the late 1980s, tech stocks at the turn of the century and in US housing before the 2008 financial crisis, GMO’s co-founder Jeremy Grantham laid out in his latest note to investors why the “super bubble” that he previously warned about hasn’t popped yet (despite this year’s somewhat chaotic market behavior).

“You had a typical bear market rally the other day and people were saying, ‘Oh, it’s a new bull market,” Grantham said in an interview with Bloomberg.

Specifically, the 83-year-old investors says that the surge in US equities from mid-June to mid-August fits the pattern of bear market rallies common after an initial sharp decline — and before the economy truly begins to deteriorate; and sees more trouble ahead because of a “dangerous mix” of overvalued stocks, bonds and housing, combined with a commodity shock and hawkishness from the Fed.

“My bet is that we’re going to have a fairly tough time of it economically and financially before this is washed through the system,’’ Grantham said.

“What I don’t know is: Does that get out of hand like it did in the ‘30s, is it pretty well contained as it was in 2000 or is it somewhere in the middle?”

In his note today, Grantham warns that we are entering the superbubble’s final act…

Two weeks ago, investing icon Jeremy Grantham turned apocalyptic and warned that the “Bursting Of This “Great, Epic Bubble” Will Be “Most Important Investing Event Of Your Lives.” Since then the market has generally continued to melt up, yet Grantham’s conviction that all this will end in tears has only grown, and in an interview with Bloomberg today, the co-founder of GMO who correctly called the last two crashes, now predicts that Joe Biden’s economic-recovery plan will propel stocks to perilous new heights, followed by an inevitable crash.

“We will have a few weeks of extra money and a few weeks of putting your last, desperate chips into the game, and then an even more spectacular bust,” the value-investing legend said in a Bloomberg “Front Row” interview.

… many veteran investors are throwing in the towel on what is emerging as the most furiously ridiculous rally in history in what is now better known as “Jay’s market” (with 73% of Wall Street claiming that the market is only up due to the artificial gimmick of the Fed’s balance sheet explosion and not due to fundamental factors). And with one after another investing legend such as Warren Buffett, Stanley Druckenmiller, David Tepper boycotting the artificial rally, and either selling or pulling out, today GMO’s Jeremy Grantham became the latest to bail on what Bank of America recently called a “fake market.”

In a letter to GMO investors, Grantham writes that “we have never lived in a period where the future was so uncertain” and yet “the market is 10% below its previous high in January when, superficially at least, everything seemed fine in economics and finance. And if not “fine,” well, good enough. The future paths include many that could change corporate profitability, growth, and many aspects of capitalism, society, and the global political scene.”

Jeremy Grantham, an investor credited with predicting the 2000 and 2008 downturns, told CNBC on Thursday that investors should get inured to lackluster returns in the stock market for the next two decades, after a century of handsome gains.

“In the last 100 years, we’re used to delivering perhaps 6%,” but the U.S. market will be delivering real returns of about 2% or 3% on average over next 20 years, the value investor and co-founder of Boston-based asset manager GMO told CNBC in a rare interview.

In late 2017, the investing legend Jeremy Grantham was officially on bubble watch.

He said as much in a quarterly letter he coauthored for his firm, Grantham, Mayo, & van Otterloo (GMO), back in December. It wasn’t an extremely pressing concern quite yet but something in the back of his mind.

That all changed in January when, as he describes it, stories of investor overconfidence became too numerous to ignore.

Grantham’s favorite anecdote came courtesy of the bus one of his Boston-based colleagues would take to work from New Hampshire. Every morning, an elderly woman would see the GMO employee reading financial literature and ask questions.

One inquiry in particular stuck out to him: Should she sell her house worth about $300,000 and put it in the stock market?

The chart below might be the most powerful indictment of the Federal Reserve and our corporate fascist empire of debt ever created. Some people don’t get charts. Charts tell a story. This chart tells the story of elitist bankers supporting the agenda of a corporate fascist state, resulting in the gutting of the middle class. Anyone who views this chart in a positive manner is either a Federal Reserve banker or their paycheck is dependent upon the continuation of the pillaging of the working class. Corporate profits are at all-time highs. Profit margins have always reverted to the mean throughout modern history. If they remain at all-time highs then something is terribly wrong.

“Profit margins are probably the most mean-reverting series in finance, and if profit margins do not mean-revert, then something has gone badly wrong with capitalism. If high profits do not attract competition, there is something wrong with the system and it is not functioning properly.”– Jeremy Grantham, Barron’s

Here is the story I see in that chart. Corporate profits as a percentage of GNP have averaged 6.5% over the last 67 years. As you can see, it is a volatile figure. Corporate profits rise during expansions and fall during recessions. That has been a given over time. The reason corporate profits have always reverted to the mean was due to the basic tenets of free market capitalism. When a company is generating outsized profits, that industry will then attract new competitors, resulting in price competition and lower profits. From 1950 through 1971, corporate profits as a percentage of GNP fluctuated in a narrow range between 5% and 7%. This was a reflection of a market driven by competition, a non-interventionist Federal Reserve, and a government not captured by corporate interests.

It is no coincidence since Nixon closed the gold window in 1971 and unleashed greedy bankers, feckless politicians, and self serving corporate executives to utilize easy money and prodigious amounts of debt to financialize our economic system and deform capitalism, corporate profits have boomed and busted. The Fed created booms and busts are clearly evident on the chart. Nixon toady Arthur Burns created an inflationary boom in corporate profits to 8% of GNP in the late 70’s followed by the collapse to 3% caused by Volcker having to raise rates to extreme levels to crush the Burns created runaway inflation.

You can see exactly when the Maestro assumed command at the Fed and proceeded to introduce the Greenspan Put, encouraging speculation, borrowing and mal-investment. His easy money boom led to the dot com bubble that doubled corporate profits from their 1987 low. Of course the profits vaporized in an instant and plunged to 4% of GNP in 2001. Greenspan and then Bernanke proceeded to drive interest rates to record lows creating a prodigious housing bubble resulting in the greatest level of mal-investment and financial fraud in world history. Corporate profits as a percentage of GNP skyrocketed from 4% to 10% in the space of six years. The banking cabal had captured the system.

The Fed orchestra kept the music playing and Wall Street kept dancing the rumba with their corporate CEO dates. The Keynesian acolytes were ecstatic. The Austrians warned of the impending bust. No one listened. The collapse of the worldwide financial system was portrayed by the corporate mainstream media, bankers like Dimon, corporate CEOs like Immelt, billionaires like Buffet, captured government bureaucrats like Paulson, and politicians like McCain and Obama, as a systematic risk that required a taxpayer rescue of criminals.

The $800 billion gift to bankers and mega-corporations by the Washington DC Party of captured politicians was chicken feed compared to the $3.5 trillion of newly printed fiat handed to Wall Street and corporate America by Bernanke and Yellen. Five years of 0% interest rates have impoverished senior citizens and savers, but they have done wonders for Wall Street and mega-corporation profits, along with executive bonuses. Corporate profits soared from 4.5% of GNP to an all-time high of 10.5% in the space of three years and have remained at this elevated level.

Who Needs Wage Earners Anyway?

Is it a coincidence that corporate profits as a percentage of GNP are at record highs while employee compensation as a percentage of GNP is at record lows? Is it a coincidence that employee compensation as a percentage of GNP peaked at 51% in 1971? That year certainly seems to be a turning point in U.S. economic history. Gold’s purpose as a check on statists, Keynesians, politicians, bankers, and the military industrial complex couldn’t be any clearer. The decline has multiple causes, but the storyline about technology being the major cause is patently false. My observations are as follows:

From the end of World War II until the mid-1970s employee compensation as a percentage of GNP was consistently between 49% and 51%. The middle class saw their standard of living rise as wages outpaced inflation, savings rates were high and led to capital investment, debt was used for long term purchases like a home or automobile, and bankers accepted deposits and made safe loans. Technological progress over the thirty years was constant, but did not result in declining wages.

From the moment Nixon closed the gold window, employee compensation as percentage of GNP relentlessly declined for the next quarter of a century from 51% to 44%. Over this time frame our economy deformed from a goods producing system driven by savings and capital investment into a service/financial economy built upon consumer debt, conspicuous consumption and market gambling. Our iconic mega-corporations fired Americans and hired Chinese slave laborers, lobbied for tax breaks, invested in their own stock, kept wage increases below the level of true inflation, and paid extravagant compensation packages to their Harvard MBA executives.

The brief upturn created by Greenspan’s irrational exuberance 90’s boom was short lived. The relentless decline resumed after the dot com collapse, even as Greenspan and Bernanke blew their epic bubble. Their financial engineering machinations on behalf of Wall Street did nothing for the average worker on Main Street. Employee compensation as a percentage of GNP declined from 47% to 44% BEFORE the financial collapse.

Unequivocal proof that Bernanke’s sole purpose of QE and ZIRP was to benefit his Wall Street owners can be seen in the continued decline from 44% to 42% since 2008. There has been no recovery for the average American. Wall Street is rolling in dough. Corporate America is rolling in dough. Politicians are rolling in dough. The average American worker is rolling in dog shit.

The mouthpieces for the Deep State insist corporate profits have reached a permanently high plateau. It’s another new paradigm. Just like 1929, 1999, and 2007. Jeremy Grantham is right. The system is broken. The inmates are running the asylum. But financial engineering will not work permanently. Baijnath Ramraika and Prashant Trivedi in their outstanding article Why Jeremy Grantham is Right about Corporate Profit Margins prove that corporate gross margins have not grown, technological advancement has not been a major factor, innovation and capital investment are non-existent, and corporate CEOs have utilized one time schemes to boost profits.

There are a few major reasons for record corporate profits. The Fed’s gift to banks and mega-corporations of zero interest rates have allowed S&P 500 corporations to refinance their existing debt and take on new debt at below market interest rates. The average interest rate paid by S&P 500 companies is now at all-time lows. Any normalization of interest rates would crush corporate profits.

Even though you hear constant propaganda from the corporate MSM, corporate CEOs, and captured politicians about the dreadful level of corporate taxes, the truth is that mega-corporations are paying record low levels of actual taxes. When profits are at record highs and tax payments at record lows you know they have captured the system. “Creative” tax avoidance and the FASB allowing banks to mark their assets to fantasy have played an enormous role in record profits.

The short term oriented casino mentality of corporate CEOs can be plainly seen in the fact depreciation expense as a percentage of revenue is at 25 year lows, resulting in short term profits but long-term decline. Instead of investing in capital to increase efficiency or expand their business, greedy myopic CEOs have chosen to buy back their own stock at all-time high prices. They did the same thing in 2005 – 2007. Driving up quarterly earnings per share to boost their own stock option compensation is how it rolls in corporate America today. Investing in their workers through higher wages isn’t even a consideration. They don’t teach that in Ivy League MBA programs. SG&A expenses as a percentage of revenue have been driven to all time lows, as outsourcing, downsizing, and working people to death have done wonders for corporate profits.

Ramraika and Trivedi reach damning conclusions of corporate America, based on their detailed unbiased research:

As the world moved increasingly towards the idea of shareholder-value maximization, time horizons for management and the shareholders have shortened. As Montier shows, the average lifespan of a company in the S&P 500 in the 1970s was about 27 years and is down to about 15 years now. In tandem, the average tenure of CEOs is down from about 10 years in the 1970s to about 6 years now. Combine this with the incentive systems prevalent today (think stock options), and it is only logical that a CEO who is going to be around for as few as six years and is going to get a large chunk of her rewards in stock options will want to see higher stock prices.

Cutting SGA expenses and postponing capital investments — actions that carry positive short-term earnings impact at the expense of a business’ competitiveness in the long-term — look promising to managers whose payoffs depend on stock prices in the short-term. Not surprisingly, the renters (there are hardly any owners any more) clamor for just such actions. The problem with this thinking is that the long-term eventually shows up. And when it does, profit margins will have no choice but to remember their long forgotten tendency to revert to mean.

Are interest rates going to be driven lower for corporations? Are taxes going to be driven lower? How many more people can corporations fire? Have economic downturns been eliminated by the Federal Reserve? Will record profits not result in increased competition and price wars? Can wages be driven even lower?

The financial, economic and political system has been captured by corporate fascist psychopaths. The Federal Reserve has aided and abetted this takeover. Their monetary manipulations have resulted in this deformity. Psychopaths always go too far. The American middle class has been murdered. Decades of declining real wages have left them virtually penniless, in debt up to their eyeballs, angry, frustrated, and unable to jump start our moribund economy by buying more Chinese produced crap. Yellen, her Wall Street puppeteers, and the corporate titans should enjoy those record profits and record stock market highs. It won’t last. Short-term profits will be wiped out, as long-term consequences always arrive when you least expect it. The artificial boom will lead to a real depression. Luckily for the oligarchs, most middle class Americans are already experiencing a depression and won’t notice the difference.

“True, governments can reduce the rate of interest in the short run. They can issue additional paper money. They can open the way to credit expansion by the banks. They can thus create an artificial boom and the appearance of prosperity. But such a boom is bound to collapse soon or late and to bring about a depression.” – Ludwig von Mises

Keep ignoring John Hussman, Robert Shiller, Jeremy Grantham, and all the other data oriented people who honestly assess the stock market and are positive we are in for a big fall. The market is so overvalued at this point that it won’t even need an external event to trigger a crash. Gravity always wins in the end.

Opinion: Being a stock-market bull just got a lot harder

The U.S. is overvalued when using many different metrics

Reuters

It’s hard to ignore the cyclically adjusted price-to-earnings ratio (CAPE) of stocks pioneered by Yale professor Robert Shiller. The CAPE has been higher only three times in the past: in 1929, 2000 and 2007.

London (MarketWatch) — Making the bullish case is getting a lot harder.

Let’s say that you want to wriggle out from underneath the bearish conclusions of the cyclically adjusted price-to-earnings ratio (CAPE), which for some time now has been very bearish. Sidestepping that conclusion turns out to be a lot harder than you think.

The CAPE is the version of the traditional P/E ratio that has been championed by Yale University finance professor (and recent Nobel laureate) Robert Shiller. Currently, for example, the CAPE stands at 25.69, which is 55% higher than its average back to the late 1800s of 16.55 and 61% higher than the ratio’s median level of 15.95. In fact, there have been only three times since the 1880s when the CAPE has been higher than where it stands today: 1929, 2000 and 2007 — all three of which, of course, coincided with major market highs.

The CAPE isn’t a perfect indicator, as Shiller himself will tell you. There are legitimate reasons to question its approach to market valuation. In addition, the bulls have shamelessly come up with myriad other “reasons” not to pay attention to it.

But Mebane Faber, chief investment officer at Cambria Investment Management, has this to say to all these so-called CAPE haters: “Fine, don’t use it. Let’s substitute in book and cash flows, two totally different metrics.”

Unfortunately for the bulls, the conclusion of looking at the market from those alternate perspectives is almost identically bearish.

Courtesy of data from Ned Davis Research, Faber ranked 43 countries’ stock markets around the world according to their relative valuations according to the CAPE as well as to cyclically adjusted ratios of price-to-book, price-to-cash flow, and price-to-dividend. When ranked according to the CAPE, for example, with top ranking going to the most undervalued country’s stock market, the U.S. is in 41st place. Only two countries are more overvalued according to this indicator.

Indicator

US market’s rank out of 43 countries, with #1 being most undervalued

CAPE

41

Cyclically-adjusted price-to-book ratio

37

Cyclically-adjusted price-to-dividend ratio

39

Cycilcally-adjusted price-to-cash-flows ratio

36

The accompanying table shows where the U.S. market would rank according to the other three indicators. Notice that ignoring the CAPE doesn’t get the bulls very far.

To argue that the U.S. stock market isn’t overvalued, in other words, the bulls not only have to dismiss the CAPE but also argue why the U.S. market should be priced so richly relative to book value, cash flows and dividends.

That’s not necessarily impossible. But it is clear that the bulls have a lot more work cut out for them.

Furthermore, even if the bearish conclusions of these diverse indicators turn out to be right, you should know that they are long-term indicators, telling you very little about the market’s near-term direction. My favorite analogy to describe the situation comes from Ben Inker, co-head of the asset-allocation team at Boston-based money management firm GMO.

He likens the market to a leaf in a hurricane: “You have no idea where the leaf will be a minute or an hour from now,” he says. “But eventually gravity will win out and it will land on the ground.”

The money manager argues that the Fed’s interventions have ruined the very recovery it was supposed to stimulate and that the market is poised to disappoint investors.

Jeremy Grantham

FORTUNE — If you hate the Federal Reserve, you have a new hero.

A few weeks ago, Jeremy Grantham, the co-founder of money management firm GMO, called newly appointed Federal Reserve chairman Janet Yellen “ignorant” in the New York Times. He also said the reason for the slow recovery was not the severe financial crisis, continued high unemployment, or the many standoffs in Washington. Instead, he blamed the Fed for ruining the recovery it was supposed to stimulate. To someone who believes in the laws of economics, it’s hard to overstate how odd that claim is. It’s positively bonkers.

Low interest rates stimulate the economy. The Fed has done everything in its power to keep interest rates down, lower and longer than anyone can remember. That should have helped the economy. And yet the recovery has been just meh. So, either Grantham is bonkers, or he is onto something. Fortune recently caught up with him to find out.

Fortune: You believe the Fed’s policies, particularly quantitative easing, have slowed the recovery. What’s your proof?

Grantham: It’s quite likely that the recovery has been slowed down because of the Fed’s actions. Of course, we’re dealing with anecdotal evidence here because there is no control. But go back to the 1980s and the U.S. had an aggregate debt level of about 1.3 times GDP. Then we had a massive spike over the next two decades to about 3.3 times debt. And GDP over that time period has been slowed. There isn’t any room in that data for the belief that more debt creates growth.

In the economic crisis after World War I, there was no attempt at intervention or bailouts, and the economy came roaring back. In the S&L crisis, we liquidated the bad banks and their bad real estate bets. Property prices fell, capitalist juices started to flow, and the economy came roaring back. This time around, we did not liquidate the guys who made the bad bets.

Can you really blame the Fed for the bailouts? That was an act of Congress.

I don’t like to get into the details. The Bernanke put — the market belief that if anything goes bad the Fed will come to the rescue — has had a profound impact on people and how they act.

Okay, but that’s still not proof that quantitative easing slowed the recovery.

There’s no proof on the other side, that the economy is any stronger from quantitative easing. There’s some indication that the crash would have been worse and the downturn would have been sharper had the Fed not stepped in, but by now the depths of that recession would have been forgotten, the system would have been healthier, and we would have regained our growth.

It’s economic doctrine that lower interest rates boost the economy. Are you saying that’s wrong?

Economic doctrine says the market is efficient. My view of the economy is not really principle-based. Higher interest rates would have increased the wealth of savers. Instead, they became collateral damage of Bernanke’s policies. The theory is that lower interest rates are supposed to spur capital spending, right? Then why is capital spending so weak at this stage of the cycle. There is no evidence at all that quantitative easing has boosted capital spending. We have always come roaring back from recessions, even after the mismanaged Great Depression. This time we are not. It’s anecdotal evidence, but we have never had such a limited recovery.

But the Fed does seem to have boosted stocks. Even if it did nothing else, doesn’t a better market help the economy?

Yes, I agree that the Fed can manipulate stock prices. That’s perhaps the only thing they can do. But why would you want to get an advantage from the wealth effect when you know you are going to have to give it all back when the Fed reverses course. At the same time, the Fed encourages steady increasing leverage and more asset bubbles. It’s clear to most investing professionals that they can benefit from an asymmetric bet here. The Fed gives them very cheap leverage on the upside, and then bails them out on the downside. And you should have more confidence of that now. The only ones who have really benefited from QE are hedge fund managers.

Okay, but then I guess that means you think stocks are going higher? I thought I had read your prediction that the market would disappoint investors.

We do think the market is going to go higher because the Fed hasn’t ended its game, and it won’t stop playing until we are in old-fashioned bubble territory and it bursts, which usually happens at two standard deviations from the market’s mean. That would take us to 2,350 on the S&P 500, or roughly 25% from where we are now.

So are you putting your client’s money into the market?

No. You asked me where the market is headed from here. But to invest our clients’ money on the basis of speculation being driven by the Fed’s misguided policies doesn’t seem like the best thing to do with our clients’ money.

We invest our clients’ money based on our seven-year prediction. And over the next seven years, we think the market will have negative returns. The next bust will be unlike any other, because the Fed and other centrals banks around the world have taken on all this leverage that was out there and put it on their balance sheets. We have never had this before. Assets are overpriced generally. They will be cheap again. That’s how we will pay for this. It’s going to be very painful for investors.

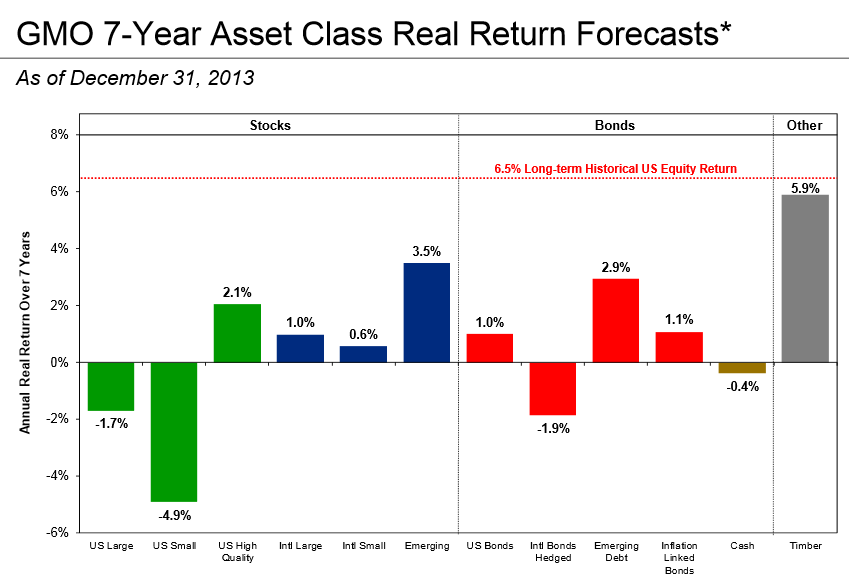

Jeremy Grantham and his bright folks at GMO, which manages billions, have just updated their 7 year return forecasts for different asset classes. They are predicting a NEGATIVE real return on stocks over the next 7 years, based on current valuations. Jim Cramer and the rest of the CNBC crowd would scoff at this outrageous prediction. Everyone knows stocks for the long run always works. Don’t fight the Fed. We’ve reached a new permanent high.

I take you back in time to yesteryear. It is December 31,1999. The Fed has been lowering interest rates in order to alleviate all of the Y2K impacts to computers and businesses around the world. Your brother in law is day trading Dot.com stocks. The stock market is hitting new highs every day. What could possible go wrong in this new and exciting internet age? Jeremy Grantham and his bright folks at GMO come out with their 10 year return forecast and predict that stocks will provide a NEGATIVE 1.9% real return over the next decade. They are laughed at and scorned. Please see the actual results versus their predictions below.

Who are you going to trust? Jeremy Grantham or Jim Cramer and his Wall Street shyster buddies?

Everyone has watched one of the best TV series of all-time – M*A*S*H. You also know the tune that played during the opening credits as helicopters delivered wounded soldiers to the 4077 Mobile Army Surgical Unit. Most people have never heard the lyrics that go with the music. The song is Suicide is Painless and the lyrics were sung during the M*A*S*H Movie. As I watched the movie a few weeks ago, the lyrics struck home. Our country has been slowly committing suicide for the last 40 years. The movie and TV series were set during the Korean War. It is fitting that military spending is one of the major causes of our suicide as a nation. On an inflation adjusted basis, the US has doubled spending on Defense since 1962. It is on course to rise another 20% in the next four years. Dwight D. Eisenhower warned us about the military industrial complex in 1961:

“In the councils of government, we must guard against the acquisition of unwarranted influence, whether sought or unsought, by the military industrial complex. The potential for the disastrous rise of misplaced power exists and will persist.”

The fact that the US currently spends 7 times as much on Defense as the next nearest country is proof that the military industrial complex has gained unwarranted influence and a disastrous rise of misplaced power has occurred.

U.S. DEFENSE SPENDING

When you critically analyze why we would need to spend 7 times as much as China on military when there is no country on earth that can challenge us, the answer can only be OIL. Our own military came to the following chilling conclusion in their Joint Operating Environment report, issued earlier this year:

By 2012, surplus oil production capacity could entirely disappear, and as early as 2015, the shortfall in output could reach nearly 10 MBD.

A severe energy crunch is inevitable without a massive expansion of production and refining capacity. While it is difficult to predict precisely what economic, political, and strategic effects such a shortfall might produce, it surely would reduce the prospects for growth in both the developing and developed worlds. Such an economic slowdown would exacerbate other unresolved tensions, push fragile and failing states further down the path toward collapse, and perhaps have serious economic impact on both China and India. At best, it would lead to periods of harsh economic adjustment. To what extent conservation measures, investments in alternative energy production, and efforts to expand petroleum production from tar sands and shale would mitigate such a period of adjustment is difficult to predict. One should not forget that the Great Depression spawned a number of totalitarian regimes that sought economic prosperity for their nations by ruthless conquest.

The U.S. military knows we are on the verge of an oil crisis. There are no new supplies ready to come on line before 2015. The President and his advisors know that an oil crisis is in our immediate future. We have military bases in Saudi Arabia, Iraq, and Kuwait. We have active fighting forces in Afghanistan and Pakistan. We have a naval armada of aircraft carriers in the Persian Gulf. Our forces completely encircle Iran. Is this a coincidence when the countries with the largest oil reserves in the world are noted?

Saudi Arabia – 262 billion barrels

Iran – 133 billion barrels

Iraq – 112 billion barrels

Kuwait – 97 billion barrels

The war on terror is a cover for access to the hundreds of billions of barrels of oil in the Middle East. A 10 million barrel per day shortfall by 2015 would be disastrous for a country that consumes 25% of all the oil in the world. Our hyper-consumer society is like a drug addict, dependent on its oil fix. If we are denied oil for even one day, the withdrawal symptoms would be traumatic and harrowing.

There are 255 million passenger vehicles in the U.S. Our society will collapse within weeks without a sufficient supply of oil. The average American’s only concern about oil is when they get a card in the mail from Jiffy Lube telling them it is time for their 5,000 mile oil change. They stick a hose in their gas tank and fluid pours out, allowing them to motor freely around mall dotted suburbia. Within five years they will be paying over $5 per gallon for this fluid or they will be waiting in lines for three hours to get 10 gallons of that precious fluid. Peak cheap oil has been predictable for decades. The Department of Energy was created 31 years ago. Preparing for peak cheap oil would have required some pain, sacrifice and forethought. But, suicide is painless.

Visions of Things To Be

Through early morning fog I see

visions of the things to be

the pains that are withheld for me

I realize and I can see…

That suicide is painless

It brings on many changes

and I can take or leave it if I please.

Suicide is Painless – M.A.S.H. Movie

As I peer through the fog and attempt to see visions of things to be, I see nothing but pain ahead. Anyone who can look at the following chart and not conclude that there is much pain ahead for this country is either a Goldman Sachs banker, a Federal Reserve Governor, or a bought off politician in Washington DC. It is no coincidence that after Richard Nixon closed the gold window in 1971 and allowed the Federal Reserve to “manage” our economy that total debt outstanding in the US surged from $2 trillion to over $50 trillion. GDP has risen by 1,300% since 1971, while total US debt has risen by 2,600%. Now for the kicker. Real GDP has only gone up by 292% since 1971. This means that 1,000% of the increase in GDP was from Federal Reserve created inflation. Over this same time frame, real wages have declined by 6%, from $318 per week in 1971 to $299 per week today. Inflation has been the American drug of choice to commit suicide over the last 40 years. It is stealthy, seemingly painless, and deadly.

Inflation is the “painless” method through which the Federal Reserve has decided this country will commit suicide. It is like turning on the car in the garage and letting the carbon monoxide slowly put you to sleep. The ruling elite are content that the American public is dumbed down by the government run public schools. They count on the fact that 9 out of 10 Americans do not understand inflation. It is an insidious scheme of robbing the working middle class and funneling it to the Wall Street/K Street ruling class. The Federal Reserve has gotten bolder in the last few years as they realized the public doesn’t understand or care what they do. Bernanke has relished in the mainstream media adulation that he saved the world with his printing press in 2008/2009. Even though critical thinkers know for a fact that it was Federal Reserve policies that created the worldwide financial conflagration in the first place, the corporate mainstream media and the Wall Street beneficiaries have been cheerleaders of Easy Al and Helicopter Ben. These men are traitors. They have purposefully impoverished senior citizens and the working middle class in order to enrich their ruling elite masters on Wall Street and in Washington DC.

Ben Bernanke on Wednesday afternoon will announce Quantitative Easing Part Deux. This is a fancy name for Ben printing $1 trillion out of thin air, buying US Treasuries and/or more toxic mortgage securities and artificially lowering interest rates to convince Americans to spend money they don’t have. Jeremy Grantham, in his recent quarterly letter, issues a scathing indictment of Bernanke’s methods:

“For all of us, unfortunately, there is still a further great disadvantage attached to the Fed Manipulated Prices. When rates are artificially low, income is moved away from savers, or holders of government and other debt, toward borrowers. Today, this means less income for retirees and near-retirees with conservative portfolios, and more profit opportunities for the financial industry; hedge funds can leverage cheaply and banks can borrow from the government and lend out at higher prices or even, perish the thought, pay out higher bonuses. This is the problem: there are more retirees and near retirees now than ever before, and they tend to consume all of their investment income. With artificially low rates, their consumption really drops. The offsetting benefits, mainly shown in dramatically recovered financial profits despite low levels of economic activity, flow to a considerable degree to rich individuals with much lower propensities to consume.”

The ruling elite in Washington DC and Wall Street decided that fraud, misinformation and cooking the books was preferable to the pain of honesty, orderly bankruptcy, and assets valued at their true worth. Ben Bernanke “saved the world” by putting the taxpayer on the hook for $1.5 trillion of toxic mortgage garbage he bought from his masters on Wall Street. John Hussman describes the decision to choose painless suicide over choosing painful medicine to cure our disease:

“Over the short run, two policies have been primarily responsible for successfully kicking the can down the road following the recent financial crisis. The first was the suppression of fair and accurate financial disclosure – specifically FASB suspension of mark-to-market rules – which has allowed financial companies to present balance sheets that are detached from any need to reflect the actual liquidating value of their assets. The second was the de facto grant of the government’s full faith and credit to Fannie Mae and Freddie Mac securities. Now, since standing behind insolvent debt in order to make it whole is strictly an act of fiscal policy, one would think that under the Constitution, it would have been subject to Congressional debate and democratic process. But the Bernanke Fed evidently views democracy as a clumsy extravagance, and so, the Fed accumulated $1.5 trillion in the debt obligations of these insolvent agencies, which effectively forces the public to make those obligations whole, without any actual need for public input on the matter.”

The Only Way to Win is Cheat

The only way to win is cheat

And lay it down before I’m beat

and to another give my seat

for that’s the only painless feat.

That suicide is painless

It brings on many changes

and I can take or leave it if I please.

Suicide is Painless – M.A.S.H. Movie

The Federal Reserve has incessantly created new bubbles every time one of their old bubbles has burst, since the elevation of Alan Greenspan as Fed Chairman in 1987. The bailout of LTCM convinced Wall Street that uncle Al would come to the rescue if their gambles endangered the financial system. Greenspan cheered on the internet revolution and flooded the system for the fake Y2K crisis. When the internet bubble burst in 2000 and the 9/11 attack struck in 2001, Greenspan aided and abetted the greatest bubble in history. He dropped interest rates to historic lows, encouraged the use of adjustable rate mortgages, didn’t enforce bank regulations, and pretended that he couldn’t see the bubble forming. Jeremy Grantham explained the Federal Reserve, Wall Street and K Street conspiracy to avoid the pain of dealing with our long-term structural problems in his latest letter:

“House prices may often not be susceptible to manipulation. Low interest rates may not be enough: they may stimulate hedge fund managers to speculate in stocks, but most ordinary homeowners are not interested in speculating. To stir up enough speculators to move house prices, we needed a series of changes, starting with increasing the percentage of the population that could buy a house. This took ingenuity on two fronts: overstating income and reducing down payment requirements, ideally to nil. This took extremely sloppy loan standards and virtually no data verification. This, in turn, took a warped incentive program that offered great rewards for quantity rather than quality, and a corporation overeager, with aggressive accounting, to book profits immediately. It also needed a much larger, and therefore new, market in which to place these low-grade mortgages. This took ingenious new packages and tranches that made checking the details nearly impossible, even if one wanted to. It took, critically, the Fed Manipulated Prices to drive global rates down. Even more importantly, it needed the global risk premium for everything to hit world record low levels so that suddenly formerly staid European, and even Asian, institutions were reaching for risk to get a few basis points more interest. Such an environment is possible only if there exists an institution with a truly global reach and a commitment to drive asset prices up. In the U.S. Fed, under the Greenspan-Bernanke regime, just such an institution was ready and willing.”

On Wednesday Ben Bernanke will inject more poison into the veins of a once great country. This country, at one time, dealt with its problems in a realistic manner and was willing to sacrifice, cooperate, and make hard choices. QE2 will not help our economy or solve any of our problems.

Is It To Be Or Not To Be?

A brave man once requested me

to answer questions that are key

‘is it to be or not to be’

and I replied ‘oh why ask me?’

‘Cause suicide is painless

it brings on many changes

and I can take or leave it if I please.

…and you can do the same thing if you choose.

Suicide is Painless – M.A.S.H. Movie

The leaders of this country, with the full support of a zombie like disinterested distracted electorate, have chosen to ignore and defer every tough decision regarding energy, spending, entitlements, deficits, and infrastructure. The Federal Reserve has allowed politicians to run the National Debt up to $13.6 Trillion by imposing no limits on the printing of fiat currency backed by nothing but promises. Based on Obama’s 10 year budget projections, adjusted for the real impact of Obamacare and extension of Bush tax cuts, the National Debt will reach $20 trillion in 2015 and $25 trillion by 2019. This is truly a suicide mission. We will never reach these levels because the sweet relief of death will overtake our economic system as the final vestiges of QE2 painlessly bring about the end.

Grantham warns that Bernanke’s actions on Wednesday are a desperate last ditch attempt to fend off the pain of reality. It will fail.

“Thus, our current policy of QE2 is merely the last desperate step of an ineffective plan to stimulate the economy through higher asset prices regardless of any future costs. Continuing QE2 may be an original way of redoing the damage done by the old Smoot-Hawley Tariff hikes of 1930, which helped accelerate a drastic global decline in trade. We may not even need the efforts of some of our dopier Senators to recreate a more traditional tariff war. And all of this stems from the Fed and the failed idea that it can or should interfere with employment levels by interfering with asset prices.”

The only difference between Dr. Bernanke and Dr. Kevorkian is that Kevorkian helped the terminally ill commit suicide. Dr. Bernanke and his colleagues at the Federal Reserve have inflicted suicide on a patient that was healthy and capable of living many more years. The suicide concoction of fiat currency, debt, military empire, and delusion has been painless for those in power, but painful for the working middle class of this country. Dr. Bernanke fancies himself as an expert on the Great Depression. He is destined to be remembered as the man who killed America. Suicide is painless, it brings on many changes.

Reuters

Reuters