The housing market peaked in 2005 and proceeded to crash over the next five years, with existing home sales falling 50%, new home sales falling 75%, and national home prices falling 30%. A funny thing happened after the peak. Wall Street banks accelerated the issuance of subprime mortgages to hyper-speed. The executives of these banks knew housing had peaked, but insatiable greed consumed them as they purposely doled out billions in no-doc liar loans as a necessary ingredient in their CDOs of mass destruction.

The millions in upfront fees, along with their lack of conscience in bribing Moody’s and S&P to get AAA ratings on toxic waste, while selling the derivatives to clients and shorting them at the same time, in order to enrich executives with multi-million dollar compensation packages, overrode any thoughts of risk management, consequences, or the impact on homeowners, investors, or taxpayers. The housing boom began as a natural reaction to the Federal Reserve suppressing interest rates to, at the time, ridiculously low levels from 2001 through 2004 (child’s play compared to the last six years).

Submitted by Tyler Durden on 07/15/2015 17:15 -0400

If you were interested in learning about the conditions that conspired to create the great American housing bubble which burst in spectacular fashion in 2008 and brought the entire global financial system to its knees, you might start by reading the history of Fannie and Freddie, or you might take a hard look at Blythe Masters and the wizards who created the credit default swap, or, if you wanted to save yourself quite a bit of time and effort, you could just look at the current market for subprime auto loans.

You see, the much maligned “originate to sell” model – which was instrumental in making the American homeownership dream a reality for underqualified borrowers in the lead up to the crisis – is alive and well and is ‘in the driver’s seat’ so to speak when it comes to auto sales in America.

As we noted last month, in the consumer ABS space (which encompasses paper backed by student loans, credit cards, equipment, auto loans, and other, more esoteric types of consumer credit) auto loan-backed issuance accounts for half of the market and a quarter of auto ABS is backed by loans to subprime borrowers.

The push to feed the securitization machine begets more competition among lenders for a shrinking pool of creditworthy borrowers and when that pool dries up, well, the definition of “creditworthy” must necessarily be relaxed, otherwise the securitization machine stalls for lack of fuel. For those who missed it, here are three charts which tell you everything you need to know about the market for auto loan-backed ABS:

Submitted by Tyler Durden on 07/11/2015 17:00 -0400

To be sure, we’ve made no secret of our views on the state of the US auto market.

This year, we’ve written extensively about the proliferation of subprime lending, worrisome trends in average loan terms, and, most recently, we noted the astounding fact that in Q4 2014, the average LTV for used vehicles hit 137%.

It seems hard to believe, but your government is purposely recreating the mortgage debacle of 2007 and putting you on the hook for the billions in losses coming down the road. In their frantic effort to generate the appearance of economic recovery they are willing to gamble with taxpayer’s money while luring unsuspecting blue collar folks into buying houses they can’t afford. During the previous housing bubble, greedy Wall Street bankers, deceitful mortgage brokers, and corrupt rating agencies colluded to commit the greatest control fraud in the history of mankind. This time it is your government, aided and abetted by the Federal Reserve, that is actively promoting the lending of money to people incapable of paying it back. And again, you the taxpayer will be on the hook when it predictably blows up.

The FHA, created during the first Great Depression, is supposed to be self-sustaining through mortgage insurance premiums charged to homeowners, just like Fannie, Freddie, Medicare, Social Security, and student loan lending were supposed to be self- sustaining through taxes, fees, and interest. This agency was supposed to promote homeownership for lower income Americans, but has been used by politicians as a tool to capture votes, payoff crony capitalist benefactors, and as a Keynesian stimulus tool designed to kindle a fake housing recovery. They entered the fray at the tail end of the last Fed/Wall Street created housing bubble, insuring a huge number of subprime mortgage loans from 2007 through 2009. The taxpayer has already had to bail out this incompetent, politically motivated, joke of an agency to the tune of $1.7 billion in 2014.

Edward J. Pinto, a former Fannie Mae official, estimates that under standard accounting practices the agency is already insolvent to the tune of $25 billion. Mark to fantasy accounting hasn’t just benefitted the criminal Wall Street cabal, but also the bloated pig government housing agencies – Fannie, Freddie and the FHA. The FHA’s share of new loans with mortgage insurance stood at 16.4% in 2005 and currently stands at 44.3%. This is a ridiculously high level considering the percentage of first time home buyers is near all-time lows and low income buyers have lower real median household income than they had in 2005. Distinguished congresswoman Maxine Waters, who once declared: “We do not have a crisis at Freddie Mac, and particularly Fannie Mae, under the outstanding leadership of Frank Raines.”, prior to them imploding and costing taxpayers $187 billion in losses, thinks the FHA is doing a bang up job. Her financial acumen is unquestioned, so you can expect another bailout in the near future.

Submitted by Tyler Durden on 03/03/2015 15:31 -0500

A running theme here has been the great rotation of bubble-blowing credit from subprime housing to subprime auto-loans. Amid government probes of underwriting standards and soaring delinquencies, it appears when the least-creditworthy Americans are cut off from debt servitude, bad things happen in car sales…

*FORD FEB. U.S. LIGHT-VEHICLE SALES FALL 2.0%, EST. UP 5.8% (miss!)

*GM FEB. U.S. AUTO SALES UP 4.2%, EST. UP 5.9% (miss!)

*NISSAN FEB. U.S. AUTO SALES UP 2.7%, EST. UP 3.8% (miss!)

*FIAT CHRYSLER FEB. U.S. AUTO SALES UP 5.6%, EST. UP 8.2% (miss!)

*HONDA FEB. U.S. AUTO SALES RISE 5%, EST. UP 11% (miss!)

*TOYOTA FEB. U.S. AUTO SALES RISE 13.3%, EST. UP 15%( miss!)

‘If you’re committed enough, you can make any story work. I once told a woman I was Kevin Costner, and it worked because I believed it’ – Saul Goodman – Breaking Bad

“As calamitous as the sub-prime blowup seems, it is only the beginning. The credit bubble spawned abuses throughout the system. Sub-prime lending just happened to be the most egregious of the lot, and thus the first to have the cockroaches scurrying out in plain view. The housing market will collapse. New-home construction will collapse. Consumer pocketbooks will be pinched. The consumer spending binge will be over. The U.S. economy will enter a recession.” – Eric Sprott – 2007

In Part One of this article I provided the background of how our current debt saturated economy got to this point of ludicrousness. The “crazy” bloggers, prophets of doom, and analysts who could do basic math were warning of an impending financial crisis in 2006 and 2007, which would be caused by the issuance of hundreds of billions in subprime slime by the Too Big To Trust Wall Street shysters. Subprime mortgages, auto loans, and credit card lines provided the kindling for the 2008 conflagration.

Under normal circumstances we wouldn’t have seen such irrational, reckless, greedy behavior from Wall Street for another generation. But, Wall Street didn’t have to accept the consequences of their actions. They were bailed out and further enriched by their puppets at the Federal Reserve, the lackey politicians they installed in Washington D.C., and on the backs of honest, hard-working, tax paying Americans. The lesson they learned was they could continue to take excessive, reckless, unregulated risks without concern for losses, downside, or consequences.

In reality, the Fed and government have worked in tandem with Wall Street to create the subprime economic recovery. The scheme has been to revive the bailed out auto industry by artificially boosting sales through dodgy, low interest, extended term debt. With the Feds taking over the entire student loan market, they have doled out hundreds of billions to kids who don’t have the educational skills to succeed in college, in order to keep them out of the unemployment calculation.

That’s why you have a 5.7% unemployment rate when 41% of the working age population (102 million people) is not working. The appearance of economic recovery has been much more important to the ruling class than an actual economic recovery for average Americans, because the .1% have made out like bandits anyway. Who has benefited from the $650 billion of student loan and auto debt disseminated by the oligarchs in the last four years, the borrowers or lenders?

I wonder who could have predicted this. Oh Yeah. Me. I wrote Subprime Auto Nation in September 2012. The entire auto recovery storyline peddled to the masses over the last few years is a sham. It’s just another Federal Reserve easy money created subprime bubble. Ally Financial and the rest of the Wall Street criminal syndicate have doled out subprime auto loans to any high school dropout that can fog a mirror, quicker than Bill Clinton does interns. The entire scheme was to give the appearance of an economic recovery and not worry about the future losses. The taxpayer would pick those up. The falsity of the fantastic auto sales meme is proven by the fact that automaker profits have fallen and their stocks are lower than they were in 2010.

Now the chickens are coming home to roost. 1 out of 12 subprime borrowers have failed to make payments within the first nine months of taking the loan. I wonder how many will make all the payments over the 7 years of their loan?

WTF did highly educated finance professionals think would happen when you loaned Shaquesha Jackson, with a 630 credit score, $40,000 to buy a Cadillac Escalade? Did they think she would make the payments with her EBT card? Did the fact she had defaulted on prior loans convince them she had learned her lesson? There are $40,000 vehicles all over West Philly, parked in front of $25,000 hovels. Who in their right mind thought lending money to these people for a rapidly depreciating vehicle was a good idea? Only an Ivy League educated Princeton economist could think this would work. Or maybe they just wanted to keep the ponzi going long enough to exit the Federal Reserve and start making $300,000 per lunchtime speech about how he saved the world.

The delinquency rates on all car loans at 2.6% are already approaching 2008 levels. I might want to remind you the government and MSM have been telling you we are in the midst of a strong economic recovery. As 2015 erodes into a greater depression, these default rates will soar well past 2008-2009 levels. The coming shitstorm created by the easy money mal-investment over the last five years is going to be epic.

Even Mark Zandi Admits It: Auto Loan “Credit Quality Is Eroding Now, And Pretty Quickly”

Submitted by Tyler Durden on 01/09/2015 10:14 -0500

The desperation of retailers grows by the day. I head to Wal-Mart and Giant in Harleysville every Sunday morning at 7:00 am. to do my weekly grocery shopping. I go to Wal-Mart at opening to avoid the freaks we see weekly on the People of Wal-Mart post. The workers at Wal-Mart are only a small step above the customers. They can barely communicate, rarely look you in the eye, and generally act like they are prisoners in an asylum.

I’m in winter/bad times ahead prep mode. I had a load of fire wood delivered yesterday which I wheelbarrowed to the back yard and stacked with my already decent sized stack. Last week I took an empty propane canister back to Wal-Mart to replace it with a full canister. That would give me three full propane tanks. I left the empty tank outside next to the propane cage and went in to pay. The old lady cashier with the gravelly smoker voice told me she would call for someone to get me a new tank.

I went over the cage and patiently waited for a Wal-Mart drone to come out, unlock the propane cage and give me a full tank. Two minutes, five minutes, and eventually ten minutes go by with no one coming out to help me. The cashier pokes her head out the door and shrugs her shoulders and says no one is responding to her calls. What a well oiled machine they have at Wal-Mart. Eventually the old lady abandoned her cashier post and in a painstakingly slow manner proceeded to unlock one bin after another until she found a full tank. I’m sure a line of unhappy customers were piling up at the only register in the garden center while she spent ten minutes getting me my propane tank.

A transaction that should have taken five minutes from start to finish ended up taking closer to twenty five minutes, with another five or six customers also dissatisfied with their extra long wait. This is a perfect example of how not to do business. Maybe Wal-Mart’s problems are bigger than households having less to spend. They are attempting to maintain their profit margins by reducing staff hours, hiring low quality people, and paying them shit wages. In the short run it may keep profits higher, but in the long-run customers will go elsewhere. Except most of the elsewhere stores closed up years ago when Wal-Mart arrived and underpriced them into bankruptcy.

My shopping experience at Giant is generally pleasant. The staff are nice, competent, and have been there for years. They know what they are doing and serve you with a smile. But their store is part of a worldwide conglomerate, so things have changed for the worse over the last four months. They renovated the entire store, creating bigger aisles and moving stuff around. That’s annoying, but after a while you figure out where they moved the stuff you want. The real negative change was the dreaded “Everyday Low Pricing”. This weasel phrase means you will be paying more. This is what the Apple idiot CEO – Ron Johnson – did at JC Penney. It put them on a rapid path to bankruptcy.

The weekly sale items at Giant have virtually disappeared. This has coincided with the drastic increase in beef, pork and fresh produce prices. Since “Every Day Low Pricing” went into affect our weekly grocery bill has gone up 20%. And I am buying far less beef and more chicken. In the past I would stock up on sale items and put beef, pork and whatever was on sale in our storage area freezer. Now I am stuck buying what we need that week. No bargains, just fully priced food items. Be forewarned, whenever you see a store announce “Everyday Low Pricing” you are getting screwed.

The Boos Begin in August & Bells Start Jingling in October

The desperation of Wal-Mart and most of the other mega-retail chains is no more clearly evident than in their relentlessly ridiculous acceleration of holiday marketing displays. I was flabbergasted when I saw Halloween candy, decorations and costumes in row after row BEFORE Labor Day at my local Wal-Mart. Selling Halloween candy two months before Halloween is idiotic and a sure sign of desperation. Retailers have run out of merchandising ideas. I wouldn’t even consider buying Halloween candy until the week before Halloween. Do Wal-Mart freaks of the week actually buy Halloween merchandise in September?

Holidays used to be special occasions that lent a sense of sales urgency for retailers for a week or two, to pump up sales. Now Wal-Mart and the rest of the dying retailers have Christmas, Easter, Fourth of July, and Halloween displays up for 80% of the year. There is no sense of urgency to buy. From September 1 though October 31 there are rows and rows of bags of corporate produced chemicals disguised as candy. I suppose the obese masses buy this crap in anticipation of Halloween, tell themselves they’ll only take one, and then shovel the entire bag down their gullets.

So last week, still a full two weeks before Halloween, Wal-Mart had already converted their entire garden center into a Christmas wonderland of cheap mass produced Chinese cookie cutter Christmas decorations and lights that will blow out after three hours of use. They had also converted aisles at the front of the store to Christmas displays. Who the hell shops for Christmas crap in October? There is nothing like having cheap Chinese Christmas crap available for over two months to create a sense of urgency to buy. Wal-Mart and the rest of the mega-retailers have got nothin. They have no original merchandising ideas. They don’t even try anymore. They source low quality goods from China and compete solely on price. I can’t wait for the Easter candy to appear on Wal-Mart’s shelves in late December.

Black Thanksgiving

Black Friday is dead. Long live Black Thanksgiving. The riots and stampedes by the ignorant masses for toasters and HDTVs on Black Friday are now being replaced by retailers and malls across America opening at 6:00 pm on Thanksgiving. It actually seems fitting. How better to give thanks for our mass consumption, debt financed, materialistic, iGadget addicted society than to open stores on Thanksgiving. Spending time with family is overrated anyway. If you had to spend six hours with cousin Eddie and aunt Bethany, you’d be looking forward to an early opening at Macy’s.

The bullshit message from the mega-retailers is: “We’re not opening on Thanksgiving out of desperation or greed. We’re doing it simply to satisfy the demands of our customers”. It’s a racist national holiday anyway. We should be going to an Indian run casino on Thanksgiving to make up for our past sins. Opening stores and forcing workers to work on Thanksgiving is pathetic, disgusting and a truly desperate measure in this consumer empire in decline. The law of diminishing returns has been invoked upon the mega-retailers that dominate our suburban sprawl paradise.

These retailers can start holiday merchandising three months before the actual holiday. They can open their doors on Thanksgiving, Easter and Christmas. It’s nothing more than shuffling the deck furniture on the Titanic. We’ve allowed bankers, politicians and corporate titans to financialize our economy, gutting the once thriving middle class, sending manufacturing jobs overseas, and convincing the clueless masses that consumer goods purchased with debt is equal to wealth. But, we’ve reached the point of no return. There are 248 million working age Americans and 102 million of them are not employed. Of the 146 million working Americans, 82 million of them make less than $30,000 per year.

While retailers have added billions of square feet since 1989, real median net worth is 5% lower over 24 years. Retailers are attempting to get blood from a stone. The stone is in debt, approaching retirement with no savings and dead broke.

We have one entity that deserves the most credit for destroying the American Dream. Real median household income is lower than it was in 1989. The 2008 collapse was caused by the easy money bubble machine at the Federal Reserve. We had the opportunity to hit the reset button, implement rational economic and monetary policies, take our lumps, and make the banking culprits pay for their crimes. Instead, the easily manipulated masses believed the Wall Street storyline and allowed the Federal Reserve and feckless politicians to save the banking cabal with extreme money printing and debt creation. This has pushed the middle class closer to the breaking point, while further enriching the oligarchs. The Federal Reserve saved their owners and lured the masses further into debt.

The Fed, Wall Street, and Washington DC have successfully driven consumer debt to an all-time high, blasting through the $3 trillion level. Declining real incomes and rising debt are a sure recipe for success.

Our entire economic paradigm is built upon desperate measures. Zero interest rates, $3 trillion of QE, systematic accounting fraud, fudged economic data, and doling out subprime loans to auto renters and University of Phoenix wannabes have failed to revive our moribund economy. Delusions don’t die easily. But they do die. We are reaching the limit of this delusionary dream built upon debt, denial, and deception. Make sure you wolf down that Thanksgiving feast before 5:00 pm. There are HDTV’s to fight for at 6:00 pm.

The MSM keeps telling me that auto sales are skyrocketing. They tout this as proof the consumer is back. Then why is Ford slashing their profit forecast by $1.5 billion? Why are their North American profit margins crashing? Why hasn’t their stock price moved at all in the last year? Why is their stock price 25% lower than it was in 2011? Why is GM’s stock price down 25% in 2014 YTD? Why is GM’s stock price still 20% lower than it was in 2011? Why are dealer lots overflowing with inventory?

The reason none of this computes is because the auto recovery is a farce. The “fantastic” sales are nothing but a debt financed bonanza created by the Fed’s easy money. Subprime financed auto”sales” are just pre-repossession gifts to deadbeats. Leases are nothing but short-term rentals to math challenged dumbasses which will be flooding dealer lots over the next few years. Even the legitimate sales are being financed at 0% for 7 years. This auto recovery is nothing but smoke and mirrors.

Ford sharply cuts full-year profit outlook

By Mike Ramsey

Published: Sept 30, 2014 8:21 a.m. ET

Just three months into the top job at Ford Motor Co., Mark Fields slashed the auto maker’s full-year profit outlook on rising troubles in emerging auto markets and costs from quality troubles and U.S. recalls.

Mr. Fields told investors on Monday the nation’s No. 2 auto maker by sales expects to report pretax profit this year of between $6 billion and $7 billion, approximately $1.5 billion less than it had forecast in July.

The largest factors: a roughly $1 billion larger tab for warranty and recall costs, a $300 million hit from declines in Russia, and a loss in South America that is $900 million larger than forecast. Better than expected unit volumes and pricing helped offset some of the shortfalls, it said.

Ford shares closed down 7.5% at $15.11 in 4 p.m. trading, the lowest close since March, and continued falling after-hours.

“The big shock today was the margin forecast given for North America,” said Brian Johnson, Barclays auto analyst. Despite high expectations for the 2015 F-150 pickup truck, Ford’s outlook for the rest of the year implies North American operating margins of between 8% and 9%, down from 11% last quarter.

The company now expects Europe to lose $1.2 billion on a pretax basis in 2014 and projects the red ink there would flow into 2015, although at a lower rate. Ford no longer expects European auto demand to return to prerecession sales levels even by 2020.

Ford also is suffering quality problems and has recalled 3.9 million U.S. vehicles so far this year, according to National Highway Traffic Safety Administration data.

Mr. Fields took over from former CEO Alan Mulally in July, and on Monday led a team of executives in laying out a road map for the business through 2020. While the company pointed out bright spots in Asia, North America and its Lincoln luxury brand,

Mr. Fields said the weak short-term outlook isn’t casting a shadow over his early days as CEO. He said the company is “looking at reality and dealing with it in a proactive way.”

(Reuters) – Strong demand drove U.S. new car and truck sales 10 percent higher in September, adding momentum to the industry’s best August in more than a decade, consultants LMC Automotive and J.D. Power said on Thursday.

Sales rose to 1.248 million new vehicles, or a seasonally adjusted annualized rate of 16.5 million vehicles. This follows a 17.5 million annualized rate in August.

“The strength in automotive sales is undeniable, as August sales performance was well above expectations and there is no evidence of a payback in September, suggesting that the auto recovery still has some legs,” LMC forecaster Jeff Schuster said.

LMC raised its full-year forecast for 2014 to 16.4 million vehicles from 16.3 million vehicles

Why have cars been so strong when housing in particular and consumer spending in general have been relatively limp? Two reasons. First, subprime lending has found a home in this market:

(New York Times) – Rodney Durham stopped working in 1991, declared bankruptcy and lives on Social Security. Nonetheless, Wells Fargo lent him $15,197 to buy a used Mitsubishi sedan.

“I am not sure how I got the loan,” Mr. Durham, age 60, said.

Mr. Durham’s application said that he made $35,000 as a technician at Lourdes Hospital in Binghamton, N.Y., according to a copy of the loan document. But he says he told the dealer he hadn’t worked at the hospital for more than three decades. Now, after months of Wells Fargo pressing him over missed payments, the bank has repossessed his car.

This is the face of the new subprime boom. Mr. Durham is one of millions of Americans with shoddy credit who are easily obtaining auto loans from used-car dealers, including some who fabricate or ignore borrowers’ abilities to repay. The loans often come with terms that take advantage of the most desperate, least financially sophisticated customers. The surge in lending and the lack of caution resemble the frenzied subprime mortgage market before its implosion set off the 2008 financial crisis.

Auto loans to people with tarnished credit have risen more than 130 percent in the five years since the immediate aftermath of the financial crisis, with roughly one in four new auto loans last year going to borrowers considered subprime — people with credit scores at or below 640.

The explosive growth is being driven by some of the same dynamics that were at work in subprime mortgages. A wave of money is pouring into subprime autos, as the high rates and steady profits of the loans attract investors. Just as Wall Street stoked the boom in mortgages, some of the nation’s biggest banks and private equity firms are feeding the growth in subprime auto loans by investing in lenders and making money available for loans.

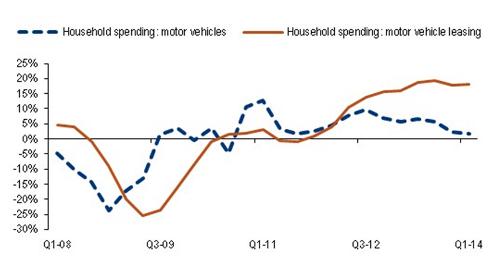

The extra demand generated by allowing (apparently) anyone with a heartbeat to buy has supported the price of used cars, making new cars more attractive by comparison. Which in turn makes leasing seem like a good deal for all concerned:

(Zero Hedge) – When it comes to signs of a US “recovery” nothing has been hyped up more than US auto companies reporting improving, in fact soaring, monthly car sales. On the surface this would be great news: with an aging car fleet, US consumers are surely eager to get in the latest and greatest product offering by your favorite bailed out car maker (at least until the recall comes). The only missing link has been consumer disposable income. So with car sales through the roof, the US consumer must be alive and well, right? Wrong, because there is one problem: it is car “sales” not sales. As the chart below from Bank of America proves, virtually all the growth in the US automotive sector in recent years has been the result of a near record surge in car leasing (where as we know subprime rules, so one’s credit rating is no longer an issue) not outright buying.

From BofA:

“Leasing soars: Household outlays on leasing are booming at a 20% yoy pace – a clear sign that demand for vehicles is alive and kicking. With average lease payments lower than typical monthly ownership costs and with a down-payment not typically required to enter into a lease, the surge in vehicle leasing is likely a sign that financial restraints are still holding back some would-be buyers. Thus, as the economy improves, bottled-up household demand for vehicles could translate to higher sales.”

Chart 1: Households go for the low capital option: leasing soars

(yoy growth rate, inflation-adjusted)

It could also translate into even higher leases, which in turn bottlenecks real, actual sales.

Of course, the problem is that leasing isn’t buying at all. It is renting, usually for a period of about 3 years. Which means that at the end of said period, an avalanche of cars is returned to the dealer and thus carmaker, who then has to dump it in the market at liquidation prices, which in turn skews the ROA calculation massively. However, what it does do is give the impression that there is a surge in activity here and now… all the expense of massive inventory writedowns three years from now.

Which is precisely what will happen to all the carmakers as the leased cars come home to roost. But what CEOs know and investors prefer to forget, is that by then it will be some other management team’s problem. In the meantime, enjoy the ZIRP buying, pardon leasing, frenzy.

(USA Today) – Used-car prices are sliding, a boon to penny-pinchers, but troubling for new-car sales.

The auto industry sales recovery in recent years means millions of used cars, many coming off lease, are starting to flood the market. The result is a decline in used-car prices that zoomed sky-high after the recession. And the decline is leading to talk that new-car auto sales growth may be peaking.

“We’re going to see a tremendous increase in used-car supply over the next couple of years,” says Larry Dominique, an executive vice president of auto-pricing site TrueCar.

That used-car cascade could dampen new-car sales in three ways:

•Less valuable trade-ins. Car shoppers may find their trade-ins are worth less than they expected when they go to buy new vehicles. That means they’ll have to shoulder larger new-car loans or forgo the purchases.

•More expensive leases. Lease rates for new vehicles are based on predicted resale value. As resale prices fall, automakers adjust predicted depreciation schedules and have to raise lease prices.

Wholesale prices were down 0.4% in August vs. a year ago, down 1.6% from July and “prices should continue to trend down as supply outpaces demand,” writes Tom Kontos of Adesa Analytical Services, which tracks wholesale prices for used cars, in a note to the industry.

At retail, the average used car sold at a franchised auto dealership went for $10,883 last month, down 1.6% from a year ago and 2.4% from July, says CNW Research.

So falling used car prices will lead to massive write-downs by the auto companies now being forced to take back all those leased vehicles. Which means the currently rosy earnings projections for GM, Ford and the other automakers playing these games are wildly overoptimistic and will have to be scaled back in an, um, unruly fashion during the next couple of years.

This sudden unpleasant surprise will come just as the Fed has ended its last round of debt monetization and is hoping that the economy will be able to grow without help. But housing, the main linchpin of the consumer economy, is already flat-lining in much of the country (see Why Isn’t Housing a Bubble?). Add the auto industry to the negative column and there won’t be many bright spots by the end of 2015. And the Fed, no matter what it says today, will have no choice but to open the spigot once more.

Thank God there are no consequences to doling out long term loans to people with bad credit in order to boost sales for a rapidly depreciating piece of machinery. This strategy never turns out bad. Right?

The size of loans for new and used cars is at an all-time high. It is now $27,500. The average monthly payment for a new vehicle, also increased $10 to $467 in Q2 2014. Over 20% of the new car loans in the last year have been to subprime deadbeat borrowers. Over 50% of all used car loans in the last year have been to subprime deadbeat borrowers. Of all new vehicles sold in Q2 2014, leases accounted for a record high 25.6 percent, up from 23.4 percent the previous year. This sure sounds like a healthy thriving auto market.

As usual, there are consequences to every dumbass action. The MSM will downplay the rising risks and the rapidly rising bad debts until the entire clusterfuck blows up “unexpectedly”. Loaning deadbeats $20,000 to $40,000 for a vehicle that depreciates by 10% when you drive it off the lot when they have no means to make a $300 to $500 per month loan payment always ends well. With loan to value ratios of 125%, repossession doesn’t pay the bills. The cracks in the dam are clearly evident. It’s beginning to spring leaks. The deluge is yet to come, but it is coming.

The total balance of loans that are 60-days delinquent has increased by $859 million since Q2 2013, while the balance of 30-day delinquent loans has increased by $2.8 billion from a year earlier. The overall automotive repossession rate saw a significant increase in the second quarter of 2014, jumping more than 70 percent to 0.62 percent from a year earlier.

I predict booming business for the repossession industry over the next three years.

U.S. consumers turn to auto loans at a record rate

By Peter Rudegeair

NEW YORKWed Sep 3, 2014 8:59am EDT

A group of Chevrolet Camaro cars for sale is pictured at a car dealership in Los Angeles, California April 1, 2014.

Credit: Reuters/Mario Anzuoni

(Reuters) – A record number of U.S. consumers are taking out loans to buy cars, especially those purchasing used vehicles, according to data released on Wednesday.

In the second quarter, 85 percent of new car purchases and 53.8 percent of used car purchases were financed, according to data from Experian Plc (EXPN.L), an information provider.

That was up 0.5 percentage points and 0.9 percentage points, respectively from the same period in 2013.

Additionally, the size of auto loan amounts and monthly payments continued to rise, especially for used cars. Since the second quarter of 2013, the average used vehicle loan rose 1.9 percent to $18,258 and the average monthly payment on such vehicles rose 1.1 percent to $355, both all-time highs.

“More and more consumers, especially those that are credit challenged, are turning to the used vehicle market as a viable option to purchase their next car,” said Melinda Zabritski, senior director of automotive finance for Experian, in a statement.

Banks were the largest lenders to consumers buying used cars, financing 35.6 percent of all such purchases, or 0.8 percentage points less than the second quarter of last year.

In recent years banks have begun to focus more on the used car market as automakers’ in-house financing arms came to dominate the new car market. Such “captive” finance companies made more than one out of every two new car loans in the second quarter, according to Experian.

Regulators have become more concerned with banks’ willingness to lengthen terms on car loans, lend to borrowers with lower credit scores and give out loans that are larger than vehicles are worth.

In addition, the U.S. Department of Justice has started investigating subprime auto loans that companies such as General Motors Co’s (GM.N) auto financing arm and Santander Consumer Holdings USA Inc (SC.N) have made and securitized since 2007.

But at least in the second quarter, the share of both new car and used car loans that went to borrowers with subprime credit scores declined, according to Experian.

“Lenders are still showing cautionary signs when lending to the subprime market and keeping their risk at manageable levels,” Zabritski said.

Wells Fargo & Co (WFC.N) remained the largest U.S. auto lender in the second quarter with a market share of 5.75 percent, down from 5.89 percent a year prior.

Capital One Financial Corp (COF.N) surged past JPMorgan Chase & Co (JPM.N) to become the third largest U.S. auto lender after Ally Financial Inc (ALLY.N). The McLean, Virginia-based bank’s share of the used car market rose from 3.77 percent to 4.20 percent.

The Wall Street shysters have no morality, conscience or humanity. They are nothing but blood sucking parasites. Their sole purpose is to enrich themselves, while impoverishing their hosts (clients & customers). They destroyed the lives of millions with their fraudulent subprime housing scheme and were bailed out by the very people they screwed. Their hubris and arrogance knows no bounds. With encouragement from their captured central bank and the Obama administration, they are resorting to subprime fraud again in an effort to revive our dead economy. It worked so well the first time with houses, it will surely work a second time with automobiles. They prey upon the ignorant, stupid, and math challenged masses.

The entire engineered auto “recovery” is nothing but an easy money debt financed fraud. It will end in tears for millions and the government will insist you bail out the bankers again.

In a Subprime Bubble for Used Cars, Borrowers Pay Sky-High Rates

Rodney Durham stopped working in 1991, declared bankruptcy and lives on Social Security. Nonetheless, Wells Fargo lent him $15,197 to buy a used Mitsubishi sedan.

“I am not sure how I got the loan,” Mr. Durham, age 60, said.

Mr. Durham’s application said that he made $35,000 as a technician at Lourdes Hospital in Binghamton, N.Y., according to a copy of the loan document. But he says he told the dealer he hadn’t worked at the hospital for more than three decades. Now, after months of Wells Fargo pressing him over missed payments, the bank has repossessed his car.

This is the face of the new subprime boom. Mr. Durham is one of millions of Americans with shoddy credit who are easily obtaining auto loans from used-car dealers, including some who fabricate or ignore borrowers’ abilities to repay. The loans often come with terms that take advantage of the most desperate, least financially sophisticated customers. The surge in lending and the lack of caution resemble the frenzied subprime mortgage market before its implosion set off the 2008 financial crisis.

Auto loans to people with tarnished credit have risen more than 130 percent in the five years since the immediate aftermath of the financial crisis, with roughly one in four new auto loans last year going to borrowers considered subprime — people with credit scores at or below 640.

The explosive growth is being driven by some of the same dynamics that were at work in subprime mortgages. A wave of money is pouring into subprime autos, as the high rates and steady profits of the loans attract investors. Just as Wall Street stoked the boom in mortgages, some of the nation’s biggest banks and private equity firms are feeding the growth in subprime auto loans by investing in lenders and making money available for loans.

And, like subprime mortgages before the financial crisis, many subprime auto loans are bundled into complex bonds and sold as securities by banks to insurance companies, mutual funds and public pension funds — a process that creates ever-greater demand for loans.

The New York Times examined more than 100 bankruptcy court cases, dozens of civil lawsuits against lenders and hundreds of loan documents and found that subprime auto loans can come with interest rates that can exceed 23 percent. The loans were typically at least twice the size of the value of the used cars purchased, including dozens of battered vehicles with mechanical defects hidden from borrowers. Such loans can thrust already vulnerable borrowers further into debt, even propelling some into bankruptcy, according to the court records, as well as interviews with borrowers and lawyers in 19 states.

In another echo of the mortgage boom, The Times investigation also found dozens of loans that included incorrect information about borrowers’ income and employment, leading people who had lost their jobs, were in bankruptcy or were living on Social Security to qualify for loans that they could never afford.

Photo

Credit

Many subprime auto lenders are loosening credit standards and focusing on the riskiest borrowers, according to the examination of documents and interviews with current and former executives from five large subprime auto lenders. The lending practices in the subprime auto market, recounted in interviews with the executives and in court records, demonstrate that Wall Street is again taking on very risky investments just six years after the financial crisis.

The size of the subprime auto loan market is a tiny fraction of what the subprime mortgage market was at its peak, and its implosion would not have the same far-reaching consequences. Yet some banking analysts and even credit ratings agencies that have blessed subprime auto securities have sounded warnings about potential risks to investors and to the financial system if borrowers fall behind on their bills.

Pointing to higher auto loan balances and longer repayment periods, the ratings agency Standard & Poor’s recently issued a report cautioning investors to expect “higher losses.” And a high-ranking official at the Office of the Comptroller of the Currency, which regulates some of the nation’s largest banks, has also privately expressed concerns that the banks are amassing too many risky auto loans, according to two people briefed on the matter. In a June report, the agency noted that “these early signs of easing terms and increasing risk are noteworthy.”

Despite such warnings, the volume of total subprime auto loans increased roughly 15 percent, to $145.6 billion, in the first three months of this year from a year earlier, according to Experian, a credit rating firm.

“It appears that investors have not learned the lessons of Lehman Brothers and continue to chase risky subprime-backed bonds,” said Mark T. Williams, a former bank examiner with the Federal Reserve.

In their defense, financial firms say subprime lending meets an important need: allowing borrowers with tarnished credits to buy cars vital to their livelihood.

Lenders contend that the risks are not great, saying that they have indeed heeded the lessons from the mortgage crisis. Losses on securities made up of auto loans, they add, have historically been low, even during the crisis.

Autos, of course, are very different than houses. While a foreclosure of a home can wend its way through the courts for years, a car can be quickly repossessed. And a growing number of lenders are using new technologies that can remotely disable the ignition of a car within minutes of the borrower missing a payment. Such technologies allow lenders to seize collateral and minimize losses without the cost of chasing down delinquent borrowers.

That ability to contain risk while charging fees and high interest rates has generated rich profits for the lenders and those who buy the debt. But it often comes at the expense of low-income Americans who are still trying to dig out from the depths of the recession, according to the interviews with legal aid lawyers and officials from the Federal Trade Commission and the Consumer Financial Protection Bureau, as well as state prosecutors.

While the pain from an imploding subprime auto loan market would be much less than what ensued from the housing crisis, the economy is still on relatively fragile footing, and losses could ultimately stall the broader recovery for millions of Americans.

Photo

Rodney Durham, 60, of Binghamton, N.Y., had his car repossessed.Credit Heather Ainsworth for The New York Times

The pain is far more immediate for borrowers like Mr. Durham, the unemployed car buyer from Binghamton, N.Y., who stopped making his loan payments in March, only five months after buying the 2010 Mitsubishi Galant. A spokeswoman for Wells Fargo, which declined to comment on Mr. Durham citing a confidentiality policy, emphasized that the bank’s underwriting is rigorous, adding that “we have controls in place to help identify potential fraud and take appropriate action.”

The Mitsubishi was repossessed last month, leaving Mr. Durham without a car. But his debt ordeal may not be over.

Some lenders go after borrowers like Mr. Durham for the debt that still remains after a repossessed car is sold, according to court filings. Few repossessed cars fetch enough when they are resold to cover the total loan, the court documents show. To get the remainder, some lenders pursue the borrowers, which can leave them shouldering debts for years after their cars are gone.

But for now, Mr. Durham, who is disabled, has a more immediate problem.

“I just can’t get around without my car,” he said.

The Brokers

Outside, the banner proclaimed: “No Credit. Bad Credit. All Credit. 100 percent approval.” Inside the used-car dealership in Queens, N.Y., Julio Estrada perfected his sales pitches for the borrowers, including some immigrants who spoke little English.

Sure, the double-digit interest rates might seem steep, Mr. Estrada told potential customers, but with regular payments, they would quickly fall. Mr. Estrada, who sometimes went by John, and sometimes by Jay, promised others cash rebates.

If the soft sell did not work, he played hardball, threatening to keep the down payments of buyers who backed out, according to court documents and interviews with customers.

The salesman was ultimately indicted by the Queens district attorney on grand larceny charges that he defrauded more than 23 car buyers with refinancing schemes.

Relatively few used-car dealers are charged with fraud. Yet the extreme example of Mr. Estrada comes as some used-car dealers — a business that has long had a reputation for aggressive pitches — are pushing sales tactics too far, according to state prosecutors and federal regulators.

And these are among the thousands of used-car dealers who are working hand-in-hand with Wall Street to sell cars. Court records show that Capital One and Santander Consumer USA all bought loans arranged by Mr. Estrada, who pleaded guilty last year. Since then, Mr. Estrada was indicted on separate fraud charges in March by Richard A. Brown, the Queens district attorney. That case is still pending.

To guard against fraud, the banks say, they vet their dealer partners and routinely investigate complaints. Capital One has “rigorous controls in place to identify any potential issues,” said Tatiana Stead, a bank spokeswoman, adding that last year “we terminated our relationship with the dealership” where Mr. Estrada worked. Dawn Martin Harp, head of Wells Fargo Dealer Services, said that “it’s important to note that not all claims of dealer fraud turn out to be fraud.”

James Kousouros, Mr. Estrada’s lawyer, said that “for those individuals for whom Mr. Estrada bore responsibility, he accepted this and is committed to the restitution agreed to.” Some civil lawsuits filed by borrowers were found to be without merit, he said.

For their part, car dealers note that like any industry they sometimes have rogue employees, but add that customers are overwhelmingly treated fairly.

“There is no place for fraud or any other nefarious activities in the industry, especially tactics that seek to take advantage of vulnerable consumers,” said Steve Jordan, executive vice president of the National Independent Automobile Dealers Association.

In their role as matchmaker between borrowers and lenders, used-car dealers wield tremendous power. They make the pitch to customers, including many troubled borrowers who often believe that their options are limited. And the dealers outline the terms and rates of the loans.

In interviews, more than 40 low-income borrowers described how they were worn down by used car dealers who kept them in suspense for hours before disclosing whether they even qualified for a loan. The seemingly interminable wait, the borrowers said, left them with the impression that the loan — no matter how onerous the terms — was their only chance.

The loans also came with other costs, according to interviews and an examination of the loan documents, including add-on products like unusual insurance policies. In many cases, the examination by The Times found, borrowers ended up shouldering loans that far exceeded the resale value of the car. A reason for that disparity is that some borrowers still owe money on cars that they are trading in when they purchase a new one. That debt is then rolled over into the new loan.

“By the end, they are paying $600 a month for a piece of junk,” said Charles Juntikka, a bankruptcy lawyer in Manhattan.

The dealers have an incentive to increase both the size and the interest rate of the loans.

The arithmetic is simple. The bigger size and rate of the loan, the bigger the dealers’ profit, or so-called markup — the difference between the rate charged by the lenders and the one ultimately offered to the borrowers. Under federal law, dealers do not have to disclose the size of the markup.

Photo

Dolores Blaylock, 51, of Austin, Tex., and her father, Fidencio Muñiz, 84. Like many buyers, she found she had unwittingly purchased an add-on — in her case, a life insurance policy.Credit Erich Schlegel for The New York Times

To buy her 2004 Mazda van, Dolores Blaylock, 51, a home health care aide in Austin, Tex., said she unwittingly paid for a life insurance policy that would cover her loan payments if she died.

Her loan totaled $13,778 — nearly three times the value of the van that she uses to shuttle her father, who uses a wheelchair, to his doctor’s appointments.

Now, Ms. Blaylock says she regrets ever buying the van, which frequently breaks down. “I am afraid to drive it out of town,” she said.

In some cases, though, the tactics veer toward outright fraud. The Times’s scrutiny of loan documents, including some produced in litigation, found that some used-car dealers submitted loan applications to lenders that contained incorrect income and employment information. As was the case in the subprime mortgage boom, it is unclear whether borrowers provided incorrect information to qualify for loans or whether the dealers falsified loan applications. Whatever the cause, the result is the same: Borrowers with scant income qualified for loans.

Mary Bridges, a retired grocery store employee in Syracuse, N.Y., said she repeatedly explained to a car salesman that her only monthly income was about $1,200 in Social Security. Still, Ms. Bridges said that the salesman falsely listed her monthly income as $2,500 on the application for a car loan submitted by a local dealer to Wells Fargo and reviewed by The Times.

As a result, she got a loan of $12,473 to buy a 2004 used Buick LeSabre, currently valued by Kelley Blue Book at around half that much. She tried to keep up with the payments — even going on food stamps for the first time in her life — but ultimately the car was repossessed in 2012, just two years after she bought it.

“I have always been told to do the responsible thing, but I said, ‘This is too much,’ ” the 76-year-old widow said.

The dealer agreed to pay Ms. Bridges $1,000 after Syracuse University law students threatened to file a lawsuit accusing the company of violating state and federal consumer protection laws.

But Wells Fargo, which resold the car for $4,500 last July, is still pursuing Ms. Bridges for $2,900 — a total that includes her remaining loan balance and an $835 fee for “cost of repossession and sale,” according to a copy of a letter that Wells Fargo sent to Ms. Bridges last August. (Wells Fargo declined to comment on Ms. Bridges.)

Photo

Shahadat Tuhin, 42, with his daughter Sadia Oishika, 10. He says his auto dealer used deceptive practices.Credit Hiroko Masuike/The New York Times

Even when authorities have cracked down on dealers, borrowers are still vulnerable to fraud. Last June, Shahadat Tuhin, a New York City taxi driver, bought a car from Mr. Estrada, the salesman in Queens who less than a year earlier had been indicted.

The charge by the Queens district attorney didn’t keep him out of the business. While his criminal case was pending, the salesman persuaded Mr. Tuhin to buy a used car for 90 percent more than the price he agreed upon. Needing the car to take his daughter, who has a heart condition, to the doctor, Mr. Tuhin said he unwittingly signed for a $26,209 loan with completely different terms than the ones he had reviewed.

Immediately after discovering the discrepancies, Mr. Tuhin, 42, said he tried to return the car to the dealership and called the lender, M&T Bank, to notify them of the fraud.

The bank told him to take up the issue with the dealer, Mr. Tuhin said.

M&T declined to comment on Mr. Tuhin, but said it no longer does business with that dealership.

The Money

Investors, seeking a higher return when interest rates are low, recently flocked to buy a bond issue from Prestige Financial Services of Utah. Orders to invest in the $390 million debt deal were four times greater than the amount of available securities.

What is backing many of these securities? Auto loans made to people who have been in bankruptcy.

An affiliate of the Larry H. Miller Group of Companies, Prestige specializes in making the loans to people in bankruptcy, packaging them into securities and then selling them to investors.

“It’s been a hot space,” Richard L. Hyde, the firm’s chief operating officer, said during an interview in March. Investors are betting on risky borrowers. The average interest rate on loans bundled into Prestige’s latest offering, for example, is 18.6 percent, up slightly from a similar offering rolled out a year earlier. Since 2009, total auto loan securitizations have surged 150 percent, to $17.6 billion last year, though some estimates have put the total volume even higher. To meet that rising demand, Wall Street snatches up more and more loans to package into the complex investments.

Much like mortgages, subprime auto loans go through Wall Street’s securitization machine: Once lenders make the loans, they pool thousands of them into bonds that are sold in slices to investors like mutual funds, pensions and hedge funds. The slices that include loans to the riskiest borrowers offer the highest returns.

Rating agencies, which assess the quality of the bonds, are helping fuel the boom. They are giving many of these securities top ratings, which clears the way for major investors, from pension funds to employee retirement accounts, to buy the bonds. In March, for example, Standard & Poor’s blessed most of Prestige’s bond with a triple-A rating. Slices of a similar bond that Prestige sold last year also fetched the highest rating from S.&P. A large slice of that bond is held in mutual funds managed by BlackRock, one of the world’s largest money managers.

Private equity firms have also seen the opportunity in auto subprime lending. A $1 billion investment by Kohlberg Kravis Roberts & Co., Centerbridge Partners and Warburg Pincus in a large subprime lender roughly doubled in about two years. Typically, it takes private equity firms three to five years to reap significant profit on their investments.

It is not just the private equity firms and large banks that are fanning the lending boom. Major insurance companies and mutual funds, which manage money on behalf of mom-and-pop investors, are also snapping up securities backed by subprime auto loans.

While there are no exact measures of how many of these loans end up on banks’ balance sheets, interviews with consumer lawyers and analysts suggest the problem is spreading, propelled by the very structure of the subprime auto market.

The vast majority of banks largely rely on dealers to screen potential borrowers. The arrangement, which means the banks rarely meet customers face to face, mirrors how banks relied on brokers to make mortgages.

In some cases, consumer lawyers say, the banks actually ignore complaints by borrowers who accuse dealers of fabricating their income or even forging their signatures.

“Even when they are presented with clear evidence of fraud, the banks ignore it,” said Peter T. Lane, a consumer lawyer in New York. “The typical refrain is, ‘It’s not our problem, take it up with the dealer.’ ”

It could quickly become the banks’ problem, analysts say, if questionable loans sour, causing losses to multiply.

For now, the banks are not pulling back. Many are barreling further into the auto loan market to help recoup the billions in revenue wiped out by regulations passed after the 2008 financial crisis.

Wells Fargo, for example, made $7.8 billion in auto loans in the second quarter, up 9 percent from a year earlier. At a presentation to investors in May, Wells Fargo said it had $52.6 billion in outstanding car loans. The majority of those loans are made through dealerships. The bank also said that as of the end of last year, 17 percent of the total auto loans went to borrowers with credit scores of 600 or less. The bank currently ranks as the nation’s second-largest subprime auto lender, behind Capital One, according to J. D. Power & Associates.

Wells Fargo executives say that despite the surge, the credit quality of its loans has not slipped. At the May presentation, Thomas A. Wolfe, the head of Wells Fargo Consumer Credit Solutions, emphasized that the overall quality of its auto loans was improving. And Tatiana Stead, the Capital One spokeswoman, said that Capital One worked “to ensure we do not follow the market to pursue growth for growth’s sake.”

Prestige says its loans experience relatively low losses because borrowers have discharged many of their other debts in bankruptcy, freeing up more cash for their car payments. Another advantage for the lender: No matter how tough things get for troubled borrowers, federal law prevents them from escaping their bills through bankruptcy for at least another seven years.

“The vast majority of our customers have been successful with their loans and leave us with a much higher credit score,” said Mr. Hyde, Prestige’s chief operating officer.

The Risks

All it took was three months.

Dolores Jackson, a teacher’s aide in Jersey City, says she thought she could handle the $540 a month on the 2012 Chevy Malibu she bought in January 2013.

But the payments on the $27,140 loan from Exeter Finance, which is owned by Blackstone, quickly overwhelmed her, and she prepared to declare bankruptcy in April.

“I was drowning,” she said.

Other borrowers have also found themselves quickly overwhelmed by car loan payments.

Even after getting a second job at Staples, Alicia Saffold, 24, a supply technician at the Fort Benning military base in Georgia, could not afford the monthly payments on her $14,288.75 loan from Exeter. The loan, according to a copy of her loan document reviewed by The Times, came with an interest rate of nearly 24 percent. Less than a year after she bought the gray Pontiac G6, it was repossessed.

Photo

Marcelina and Jonathan Mojica, and their dog, Lilly. “The car gets more money than what we put in our fridge,” Mr. Mojica said.Credit Damon Winter/The New York Times

In the case of Marcelina Mojica and her husband, Jonathan, they are keeping up with their payments on their $19,313.45 Wells Fargo auto loan — but just barely. They are currently living in a homeless shelter in the Bronx.

“The car gets more money than what we put in our fridge,” said Mr. Mojica, 28. Such examples of distress underscore the broader strains within the subprime auto loan market.

Exeter Finance declined to comment on Ms. Saffold or Ms. Jackson, but Blackstone, its parent company, emphasized that the credit quality of its lender’s loans was improving and that it worked hard to ensure its customers received the best rates. To ensure the accuracy of loan documents, Blackstone said, employees vet both dealers and borrowers.

“Exeter Finance believes it’s important to provide people with the option to finance transportation essential to their livelihood,” said Mark Floyd, the company’s chief executive.

Still, financial firms are beginning to see signs of strain. In the first three months of this year, banks had to write off as entirely uncollectable an average of $8,541 of each delinquent auto loan, up about 15 percent from a year earlier, according to Experian.

Some investors think the time is right to start selling their holdings. Earlier this year, for example, private equity firms, including K.K.R., sold most of their stake in the subprime auto lender, Santander Consumer USA, when the lender went public. Since the company’s initial public offering, the stock has fallen more than 16 percent.

While losses from soured car loans would be far less than those on subprime mortgages, the red ink could still deal a blow to the banks not long after they recovered from the housing bust. Losses from auto loans might also cause the banks to further retrench from making other loans vital to the economic recovery, like those to small business and would-be homeowners.

In another sign of trouble ahead, repossessions, while still relatively low, increased nearly 78 percent to an estimated 388,000 cars in the first three months of the year from the same period a year earlier, according to the latest data provided by Experian. The number of borrowers who are more than 60 days late on their car payments also jumped in 22 states during that period.

As a result, some rating agencies, even those that had blessed auto loan securitizations with high ratings, are starting to question the quality of the loans backing those securities, and warn of losses that investors could suffer if the bonds start to sour. Describing the potential trouble ahead, Kevin Cole, an analyst with Standard & Poor’s, said, “We believe these trends could lead to higher losses and weakened profitability in a few years.”

If those losses materialize, they could pummel a wide range of investors, from pension funds to insurance companies to mutual funds held by Americans preparing for retirement. For the huge baby-boomer generation, including many whose savings were sapped by the 2008 crisis and the ensuing recession, any losses from the auto loan securities could deal them another setback.

“Borrowers are haunted by this debt, and it can crater their credit scores, prevent them from getting other loans and thrust them even further onto the financial margins,” said Ahmad Keshavarz, a consumer lawyer in New York.

Some borrowers are stuck making payments on loans that were fraudulently made by dealers, according to an examination of dozens of lawsuits against dealers. There are no exact measures of just how many people whose cars have been repossessed end up in this predicament, but lawyers for borrowers say that it is a growing problem, and one that points to another element of subprime auto lending.

Thanks to an amendment to the Dodd-Frank financial overhaul, the vast majority of dealers are not overseen by the Consumer Financial Protection Bureau. Since its start in 2010, the agency has earned a reputation for aggressively penalizing lenders, but it has limited authority over dealers.

The Federal Trade Commission, the agency that does oversee the dealers, has cracked down on certain questionable practices. And although the agency has won a number of cases against dealers for failing to accurately disclose car costs and other abuses, it has not taken aim at them for falsifying borrowers’ incomes, for example.

Photo

Alicia Saffold, 24, received a loan with an interest rate of nearly 24 percent. Her car was soon repossessed.Credit Tami Chappell for The New York Times

And the help is not coming fast enough for borrowers like Mr. Durham, the retiree in Binghamton; Mr. Tuhin, the taxi driver in Queens; or Ms. Saffold, the technician in Georgia.

“Buying the car was the worst decision I have ever made,” Ms. Saffold said.

I wrote Subprime Auto Nation in September of 2012. GM and the rest of the slimeball auto industry utilized the free money being pumped out by the Federal Reserve to hawk their vehicles to every LeBron, Lakeisha, and Jamal in West Philly and the rest of Obama Welfare Nation with subprime auto loans out the yazoo. What could possibly go wrong providing seven year financing on $40,000 Cadillacs to people without jobs, without prospects, with sub 100 IQs, and long histories of defaulting on loans?

Considering Ally Financial, the number one dispenser of this subprime slime, was owned by Obama and the Feds until a few months ago, you have your answer. They used your tax money to get their voters in the latest models from that QUALITY IS OPTIONAL Government Motors union loving car company that has recalled more cars in the last few months than it sold in the previous two years.

Do you find it interesting that Obama and his minions, along with their co-conspirators on Wall Street decided to IPO Ally Financial back to the public just as the bad debt was beginning to roll in on this subprime slime? The underwriters for this joke of a company were Citigroup, Goldman Sachs, Morgan Stanley and Barclays Capital.

Wall Street has packaged these worthless pieces of paper into derivative sacks of shit and sold them to their clients, little old ladies, and pension funds. Does this ring a bell? They’ve done exactly what they did with subprime mortgages. EXACTLY. It worked so well the first time.

Now the shit is being fed into the fan. Guess who will be sprayed with the shit.

Sub-Prime Car Loans See a ‘Sudden Jump in Late Payments’

We have commented a few times on the slightly diffuse character of the echo bubble, which has infected a great many nooks and crannies of the economy. One of the areas which has experienced an enormous boom was the sub-prime auto loan sector. It seems however that the party in this sub-sector of the bubble economy is in the process of ending.

“A three-year lending boom to car buyers with spotty credit that helped push auto sales to a six-year high is starting to show signs of overheating.

The percentage of loans packaged into securities that are more than 30 days late rose 1.43 percentage points to 7.59 percent in the 12 months ended September 30, according to Standard & Poor’s. That’s the highest in at least three years, the data released last week by the New York-based ratings company show.

“We’re at this inflection point,” Amy Martin, an analyst at S&P, said by telephone. “Now that they are opening the lending spigot, it’s only natural that losses are starting to rise.”

Underwriting standards began to decline amid five years of Federal Reserve stimulus that set off a race for higher-yielding assets, spurring a surge in issuance of bonds tied to subprime auto loans. That breathed life into a car-finance business that had contracted in the wake of the credit crisis, attracting new lenders and private-equity firms such as Blackstone Group LP with cheap funding and high margins.

Delinquencies on subprime auto loans are likely to have increased more during the fourth quarter, the holiday period when consumers typically stretch their budgets, according to S&P. That’s poised to increase losses that bondholders will take from defaults on the debt, which stood at 6.92 percent at the end of September after falling to as low as 4.15 percent in 2011, S&P data show.

“Many lenders have told us that their performance in recent years exceeded their expectations,” Martin wrote in a report last month. “We are now hearing that they expect losses to trend upward to more normal levels this year and next.”

[…]

Subprime lenders have found cheap funding in the bond market, with $17.6 billion of asset-backed securities tied to subprime auto loans issued last year, more than double the $8 billion sold in 2010, according to Barclays Plc. About $3.6 billion of the securities have been offered this year, according to data compiled by Bloomberg.

(emphasis added)

We wonder of there is any pie Blackstone doesn’t have a finger in these days… Anyway, it seems investors in these loans – after enjoying above average returns for a good while – must now brace for growing losses. That ‘underwriting standards have declined’ is really no surprise – that is what happens when the Federal Reserve prints wagon-loads of money and pressures short term interest rates to zero. In fact, this decline in lending standards was arguably one of the main goals of the policy.

It Always Starts Somewhere …

However, what interests us about this development is mainly this: it shows that the credit bubble is beginning to fray at the edges. Every downturn starts with a seemingly innocuous report about things ‘suddenly’ and ‘unexpectedly’ going wrong in a relatively obscure corner of the market. We find ourselves reminded of how sub-prime real estate credit troubles began to show up for the first time in February of 2007, leading to the often repeated mantra that this particular disturbance in the force was ‘well contained’.

That is however never how it works – in the end, it is all one big interconnected market. When troubles begin to show up at one end of it, they soon tend to begin to spread.

A car repo notice – at least the repo sector can expect a boom now.

Good-bye overpriced SUV piece of junk – it was nice to know ye while it lasted …

Conclusion:

One should certainly keep both eyes open henceforth; more anecdotal evidence of this type is likely to emerge in coming months, especially if the Fed continues with its ‘QE tapering’ course. Once problems become visible in one obscure corner of the low grade credit markets, it is often a warning sign for the entire market and economy.

The definition of death rattle is a sound often produced by someone who is near death when fluids such as saliva and bronchial secretions accumulate in the throat and upper chest. The person can’t swallow and emits a deepening wheezing sound as they gasp for breath. This can go on for two or three days before death relieves them of their misery. The American retail industry is emitting an unmistakable wheezing sound as a long slow painful death approaches.

It was exactly four months ago when I wrote THE RETAIL DEATH RATTLE. Here are a few terse anecdotes from that article:

The absolute collapse in retail visitor counts is the warning siren that this country is about to collide with the reality Americans have run out of time, money, jobs, and illusions. The exponential growth model, built upon a never ending flow of consumer credit and an endless supply of cheap fuel, has reached its limit of growth. The titans of Wall Street and their puppets in Washington D.C. have wrung every drop of faux wealth from the dying middle class. There are nothing left but withering carcasses and bleached bones.

Once the Wall Street created fraud collapsed and the waves of delusion subsided, retailers have been revealed to be swimming naked. Their relentless expansion, based on exponential growth, cannibalized itself, new store construction ground to a halt, sales and profits have declined, and the inevitable closing of thousands of stores has begun.

The implications of this long and winding road to ruin are far reaching. Store closings so far have only been a ripple compared to the tsunami coming to right size the industry for a future of declining spending. Over the next five to ten years, tens of thousands of stores will be shuttered. Companies like JC Penney, Sears and Radio Shack will go bankrupt and become historical footnotes. Considering retail employment is lower today than it was in 2002 before the massive retail expansion, the future will see in excess of 1 million retail workers lose their jobs. Bernanke and the Feds have allowed real estate mall owners to roll over non-performing loans and pretend they are generating enough rental income to cover their loan obligations. As more stores go dark, this little game of extend and pretend will come to an end.

Retail store results for the 1st quarter of 2014 have been rolling in over the last week. It seems the hideous government reported retail sales results over the last six months are being confirmed by the dying bricks and mortar mega-chains. In case you missed the corporate mainstream media not reporting the facts and doing their usual positive spin, here are the absolutely dreadful headlines:

Wal-Mart Profit Plunges By $220 Million as US Store Traffic Declines by 1.4%

Target Profit Plunges by $80 Million, 16% Lower Than 2013, as Store Traffic Declines by 2.3%

Sears Loses $358 Million in First Quarter as Comparable Store Sales at Sears Plunge by 7.8% and Sales at Kmart Plunge by 5.1%

JC Penney Thrilled With Loss of Only $358 Million For the Quarter

Kohl’s Operating Income Plunges by 17% as Comparable Sales Decline by 3.4%

Costco Profit Declines by $84 Million as Comp Store Sales Only Increase by 2%

Staples Profit Plunges by 44% as Sales Collapse and Closing Hundreds of Stores

Gap Income Drops 22% as Same Store Sales Fall

Ann Taylor Profit Crashes by 75% as Same Store Sales Fall

American Eagle Profits Tumble 86%, Will Close 150 Stores

Aeropostale Losses $77 Million as Sales Collapse by 12%

Big Lots Profit Tumbles by 90% as Sales Flat & Exiting Canadian Market

Best Buy Sales Decline by $300 Million as Margins Decline and Comparable Store Sales Decline by 1.3%

Macy’s Profit Flat as Comparable Store Sales decline by 1.4%

Dollar General Profit Plummets by 40% as Comp Store Sales Decline by 3.8%

Urban Outfitters Earnings Collapse by 20% as Sales Stagnate

McDonalds Earnings Fall by $66 Million as US Comp Sales Fall by 1.7%

Darden Profit Collapses by 30% as Same Restaurant Sales Plunge by 5.6% and Company Selling Red Lobster

TJX Misses Earnings Expectations as Sales & Earnings Flat

Dick’s Misses Earnings Expectations as Golf Store Sales Plummet

Home Depot Misses Earnings Expectations as Customer Traffic Only Rises by 2.2%

Lowes Misses Earnings Expectations as Customer Traffic was Flat

Of course, those headlines were never reported. I went to each earnings report and gathered the info that should have been reported by the CNBC bimbos and hacks. Anything you heard surely had a Wall Street spin attached, like the standard BETTER THAN EXPECTED. I love that one. At the start of the quarter the Wall Street shysters post earnings expectations. As the quarter progresses, the company whispers the bad news to Wall Street and the earnings expectations are lowered. Then the company beats the lowered earnings expectation by a penny and the Wall Street scum hail it as a great achievement. The muppets must be sacrificed to sustain the Wall Street bonus pool. Wall Street investment bank geniuses rated JC Penney a buy from $85 per share in 2007 all the way down to $5 a share in 2013. No more needs to be said about Wall Street “analysis”.

It seems even the lowered expectation scam hasn’t worked this time. U.S. retailer profits have missed lowered expectations by the most in 13 years. They generally “beat” expectations by 3% when the game is being played properly. They’ve missed expectations in the 1st quarter by 3.2%, the worst miss since the fourth quarter of 2000. If my memory serves me right, I believe the economy entered recession shortly thereafter. The brilliant Ivy League trained Wall Street MBAs, earning high six digit salaries on Wall Street, predicted a 13% increase in retailer profits for the first quarter. A monkey with a magic 8 ball could do a better job than these Wall Street big swinging dicks.

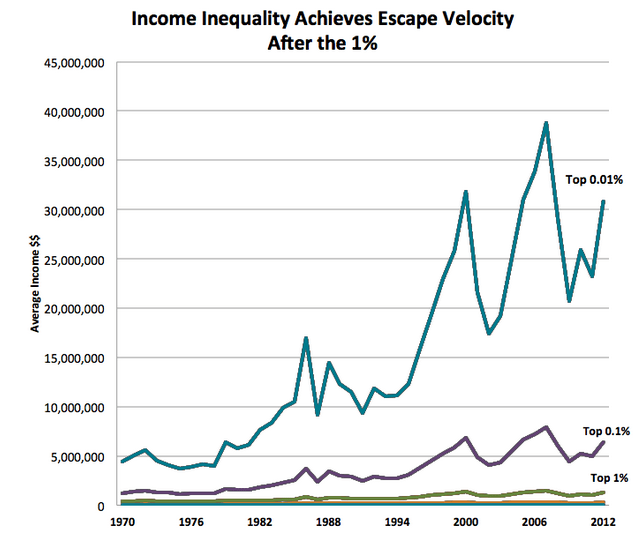

The highly compensated flunkies who sit in the corner CEO office of the mega-retail chains trotted out the usual drivel about cold and snowy winter weather and looking forward to tremendous success over the remainder of the year. How do these excuse machine CEO’s explain the success of many high end retailers during the first quarter? Doesn’t weather impact stores that cater to the .01%? The continued unrelenting decline in profits of retailers, dependent upon the working class, couldn’t have anything to do with this chart? It seems only the oligarchs have made much progress over the last four decades.

Retail CEO gurus all think they have a master plan to revive sales. I’ll let you in on a secret. They don’t really have a plan. They have no idea why they experienced tremendous success from 2000 through 2007, and why their businesses have not revived since the 2008 financial collapse. Retail CEOs are not the sharpest tools in the shed. They were born on third base and thought they hit a triple. Now they are stranded there, with no hope of getting home. They should be figuring out how to position themselves for the multi-year contraction in sales, but their egos and hubris will keep them from taking the actions necessary to keep their companies afloat in the next decade. Bankruptcy awaits. The front line workers will be shit canned and the CEO will get a golden parachute. It’s the American way.

The secret to retail success before 2007 was: create or copy a successful concept; get Wall Street financing and go public ASAP; source all your inventory from Far East slave labor factories; hire thousands of minimum wage level workers to process transactions; build hundreds of new stores every year to cover up the fact the existing stores had deteriorating performance; convince millions of gullible dupes to buy cheap Chinese shit they didn’t need with money they didn’t have; and pretend this didn’t solely rely upon cheap easy debt pumped into the veins of American consumers by the Federal Reserve and their Wall Street bank owners. The financial crisis in 2008 revealed everyone was swimming naked, when the tide of easy credit subsided.