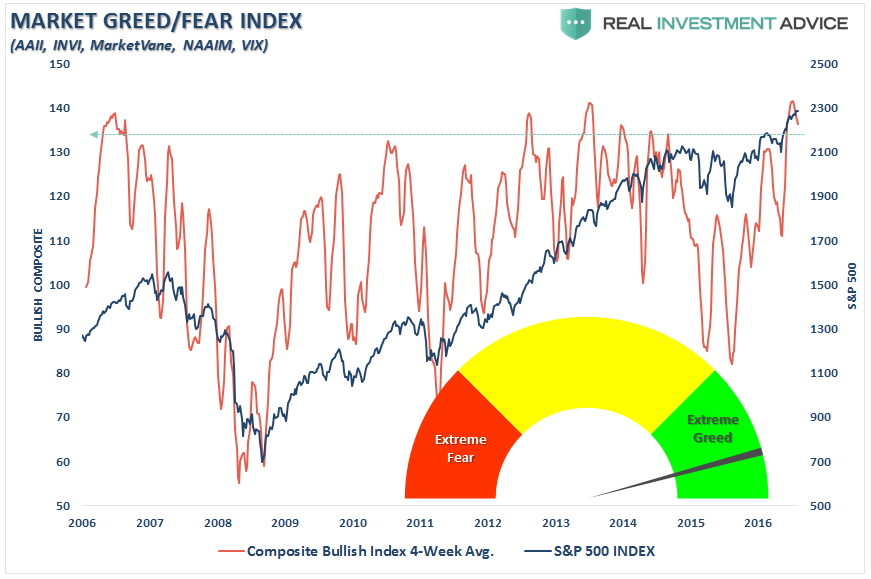

John Hussman with more facts for you to ignore. The market is going to crash. It might be a Greek default, a Chinese bubble bursting, or a Wall Street hedge fund blowing up. It’s always something. If it’s not one thing, it’s another.

Much of the investment world seems to view present conditions as a “Goldilocks market” where economic growth is positive enough to avoid recession, but not fast enough to provoke the Federal Reserve to hike interest rates. Even if these views on economic growth and Federal Reserve policy are correct, it hardly follows that stock prices will advance. S&P 500 returns are only weakly correlated with year-over-year GDP growth and have near-zero correlation with year-over-year changes in earnings. Likewise, the stance of the Federal Reserve has much less power to distinguish investment outcomes than investors seem to believe, which they might realize even by remembering that the Fed was easing aggressively and persistently throughout the 2000-2002 and 2007-2009 market collapses.

In contrast, we find profound differences in market outcomes across history depending on the combined status of valuations, market internals, and broader measures of market action (which include, for example, overvalued, overbought, overbullish syndromes). Some of these combinations, from most to least favorable, are:

1) Favorable valuations that are newly joined by a shift to favorable market internals;

2) Unfavorable valuations, coupled with favorable market internals, and without overvalued, overbought, overbullish features – which is an environment where speculation is reasonable;

3) Favorable valuations but without favorable market internals – where we observe positive average market returns but higher variability than in any other classification;

4) Unfavorable valuations, favorable market internals, but the emergence of overvalued, overbought overbullish features – which typically results in what I call “unpleasant skew”: a tendency toward persistent, marginal new highs, punctuated by “air pockets” that can wipe out weeks or months of progress in a handful of sessions, though the risk of a deeper crash becomes significant only after market internals also deteriorate;

5) Unfavorable valuations and unfavorable market internals, coming off of a recent period of overvalued, overbought, overbullish conditions – which represents the most severe return/risk profile we identify, and captures the bulk of historical market crashes.

Continue reading “The Roseanne Roseannadanna market”