Click to visit the TBP Store for Great TBP Merchandise

A mere quarter percentage point rate increase by the Federal Reserve might seem small and gradual, but for millions of consumers with credit card debt it will be stinging.

In a report this week, WalletHub analyzed data and found that U.S. consumers have been piling on credit card debt at an alarming pace, adding $92 billion in new debt last year alone—twice the postrecession average.

Lenders so far seem only too happy to extend credit, thanks to low levels of defaults and charge-offs, but the day of reckoning is coming, warns WalletHub.

“Only four times in the past 30 years have we spent so much in a year. And in each of those prior cases, the charge-off rate—currently hovering near historic lows—rose the following year,” said WalletHub.

“Once you strip out the effects of the debt binge, the artificial stimulus via currency depreciation, and the fabled ‘wealth effect’ from the equity market runup, real GDP growth stripped-down to its core was the grand total of 0.7% last year. Potemkin would be proud.” – David Rosenberg

It appears every president finds the religion of false economic narrative once they ascend to power. Trump never stops babbling and tweeting about the fantastic economy and raging jobs market since his election. He has embraced the stock market bubble as proof of his brilliant leadership, rather than the tens of trillions in debt propping up the most overvalued market in world history. Every president takes credit for any good news, spins bad news as good news, or blames the previous president for bad news that can’t be denied. The president has absolutely zero impact on the economy or stock market over the short term. It’s like taking credit for the sun rising in the east each morning.

The Big Lie method works wonders when you have a willfully ignorant, mathematically challenged, easily manipulated populace. I spent the entire Obama presidency obliterating the fake economic data perpetuated by his BLS, BEA and every other government agency trying to paint a rosy economic picture. I voted for Trump because the thought of Crooked Hillary as the president made me ill. Despite disagreeing with many of his economic, budgetary, and military policies during his first year in office, I’d vote for him again over Hillary in an instant. The thought of having that evil shrew running the country gives me chills.

Could the house of credit cards Americans have built be on the verge of collapse?

Earlier this week, the New York Fed released the latest data on US household debt, revealing it has grown to a record $13 trillion. Americans have been spending, but they’ve been putting a lot of it on plastic. Credit card balances grew by $24 billion in the last quarter of 2017 alone. Meanwhile, US consumers owe $1.22 trillion on vehicle loans. This can only go on for so long. And their are indications that the American credit card spending spree may be winding down.

Retail sales unexpectedly fell in January, recording their biggest drop in nearly a year.

It’s official: the reason behind the recent rebound in the economy can be explained with two words: “charge it.”

Readers may recall that one month ago, we reported that with Republicans in Washington on the verge of passing their first major piece of legislation in the form of comprehensive tax cuts that will allow Americans across the income spectrum to keep a little more of their hard earned cash in 2018, it appeared that U.S. consumers already “pre-spent” their savings using their credit cards.

And now we have confirmation that this is precisely what happened, because in the month of November, between revolving, or credit card, and non-revolving debt, largely student and auto loans, according to the latest Fed data, total consumer debt rose by $28 billion, or the most since November 2001, to $3.827 trillion, an annualized increase of 8.8%, or roughly 4 times faster than the pace of overall GDP growth.

With Republicans in Washington D.C. on the verge of passing their first major piece of legislation in the form of comprehensive tax cuts that will allow Americans across the income spectrum to keep a little more of their hard earned cash in 2018, it appears as though eager U.S. consumers may have already “pre-spent” their savings on their credit cards.

As the folks at Gluskin Sheff point out, 13-week annualized credit card balances in the U.S. have gone completely vertical in the last few months of 2017 which should make for some great Christmas gifts for little Johnny and Susie…gifts that will undoubtedly find themselves tucked away in a dark closet, never to be seen again, by mid January.

Donald Trump tells me our best days are ahead. Once his tax cut plan is passed, the future will be so bright I’ll have to wear shades.

Sometimes a single chart reveals the truth being obscured by the Deep State propaganda machine, working overtime selling their economic recovery narrative. The economy most certainly is booming for Wall Streeters and D.C. parasites sucking on the teet of Federal government largess. But for the average working deplorable, this supposed recovery has passed them by.

The cognitive dissonance is strong, as average Americans want to believe what their “leaders” are telling them to believe, but their personal financial situation contradicts the narrative. Even using the highly manipulated data peddled by the BLS, any critical thinking individual can see through the lies, misinformation and bullshit.

“The principle of spending money to be paid by posterity, under the name of funding, is but swindling futurity on a large scale.” ― Thomas Jefferson

Yesterday the government reported a “modest” August budget deficit of $108 billion. That’s one month folks. This is another example of how the government and their mainstream media mouthpieces portray horrifically bad, extremely abnormal financial data as normal and expected. They pretend everything that has happened since 2008 is just standard operating procedure. They follow the Big Lie theory to the extreme. The masses have been so dumbed down, desensitized, and taught to believe delusions, they can’t distinguish the abnormal from the normal.

I stopped trying to predict markets back in 2008 when the Federal Reserve, Treasury Department, Wall Street bankers, and their propaganda peddling media mouthpieces colluded to rig the markets to benefit the elite establishment players while screwing average Americans. I haven’t owned any stocks to speak of since 2006. I missed the the final blow-off, the 50% crash, and the subsequent engineered new bubble. But that doesn’t stop me from assessing our true economic situation, market valuations, and historical comparisons in order to prove the irrationality and idiocy of the current narrative.

The proof of this market being rigged and not based upon valuations, corporate earnings, discounted cash flows, or anything related to free market capitalism, was the reaction to Trump’s upset victory. The narrative was status quo Hillary was good for markets and Trump’s anti-establishment rhetoric would unnerve the markets. When the Dow futures plummeted by 800 points on election night, left wingers like Krugman cackled and predicted imminent collapse. The collapse lasted about 30 minutes, as the Dow recovered all 800 points and has subsequently advanced another 1,500 points since election day. Krugman’s predictive abilities proven stellar once again.

The mainstream media mouthpieces for the establishment peddle false narratives, disingenuous storylines, and outright propaganda to keep the ignorant masses confused, oblivious to reality, misinformed, and passively submissive to the opinions of highly paid “experts” and captured fiscal authorities. The existing social order likes things just as they are.

They reap ill-gotten riches, wield unchecked power, and control the minds of the masses. They are the invisible government consciously manipulating the minds, habits and opinions of the multitudes in order to dominate society, control the levers of government, and accumulate obscene levels of wealth through manipulation of the currency and domination of the banking and corporate interests.

One of the false narratives being flogged by the establishment propaganda peddlers is the mass retirement of Baby Boomers causing the plunge in the employment to population rate from 64.4% in 2000 to 59.7% today. They need to peddle this drivel, because the difference between these two rates amounts to 12 million missing jobs. The employment to population ratio is currently at 1984 levels. Any critical thinking person with basic math skills realizes the government reported unemployment rate of 5% is an Orwellian farce.

Deferred gratification is an unknown concept to most Americans. Wall Street and Madison Avenue have colluded to brainwash a dumbed down populace into going into perpetual debt in order to keep up with the Joneses and live for today. Saving for the future is for suckers. When 65% of Americans roll a credit card balance at 10% to 25% interest, you know our government run public educational system has succeeded in producing brain dead dumbasses. Charge!!!!

Credit cards are an addiction that most Americans never shake.

Through the booms, busts, and recessions of the last 15 years, U.S. credit habits have been remarkably consistent, according to a recent study from the Federal Reserve Bank of Boston. Most people carry over a balance from month to month, the study said, and they eagerly gobble up any additional credit their card-issuers offer.

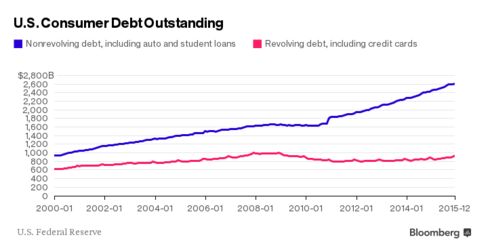

It adds up fast. Consumers owed a total of $936 billion in credit-card and other revolving debt in December, according to Federal Reserve data released on Feb. 5. They’ve added $103 billion since April 2011, but they still have less revolving debt than just before the financial crisis in 2008, when they owed $1.02 trillion.

To see how individual Americans’ relationships to credit cards has changed through time, researchers at the Boston Fed’s Consumer Payments Research Center analyzed a huge data set, a sample of 5 percent of U.S. credit report accounts from 2000 to 2014. Here are some findings:

1. The Typical American Is Always in Credit-Card Debt

About 35 percent of those aged 25 to 50 with credit cards are “convenience users,” who pay off their balances each month. The majority, whom researchers call “revolvers,” carry debt forward from month to month and usually pay high interest charges in the process.

Americans don’t really taper their credit-card borrowing until their fifties. Even at age 70, 45 percent of credit-card users aren’t paying off their credit cards each month. And the typical 80-year-old still has more than $600 on a credit card. “The median person is always borrowing, although at the end of life she is not borrowing much,” the study concludes.

“Above all, don’t lie to yourself. The man who lies to himself and listens to his own lie comes to a point that he cannot distinguish the truth within him, or around him, and so loses all respect for himself and for others. And having no respect he ceases to love.” – Fyodor Dostoyevsky, The Brothers Karamazov

The lies we tell ourselves are only exceeded by the lies perpetrated by those controlling the levers of our society. We’ve lost respect for ourselves and others, transforming from citizens with obligations to consumers with desires. The love of mammon has left our country a hollowed out, debt ridden shell of what it once was. When I see the data from surveys about the amount of debt being carried by people in this country and match it up with the totals reported by the Federal Reserve, I’m honestly flabbergasted that so many people choose to live a lie. By falling for the false materialistic narrative of having it all today, millions of Americans have enslaved themselves in trillions of debt. The totals are breathtaking to behold:

Total mortgage debt – $13.6 trillion ($9.9 trillion residential)

Total credit card debt – $924 billion

Total auto loan debt – $1.0 trillion

Total student loan debt – $1.3 trillion

Other consumer debt – $300 billion

With 118 million occupied households in the U.S., that comes to $145,000 per household. But, when you consider only 74 million of the households are owner occupied and approximately 26 million of those are free and clear of mortgage debt, that leaves millions of people with in excess of $200,000 in mortgage debt. Keeping up with the Joneses has taken on a new meaning as buying a 6,000 sq ft McMansion with 3% down became the standard operating procedure for a vast swath of image conscious Americans. When you are up to your eyeballs in debt, you don’t own anything. You are living a lie.

Two recent surveys, along with numerous other studies and data, reveal most American households to be living on the brink of catastrophe, but continuing to act in a reckless and delusionary manner. There have certainly been economic factors beyond the control of average Americans that have resulted in real median household incomes remaining stagnant for the last 36 years. The unholy alliance of mega-corporations, Wall Street and bought off corrupt politicians have gutted the nation of millions of good paying jobs under the guise of globalization, while utilizing debt, derivatives and financial schemes to enrich themselves. The malfeasance of the sociopathic privileged class does not discharge the personal responsibility of citizens for living within their means. A lack of discipline, inability to delay gratification, failure to understand basic mathematical concepts, materialistic envy, absence of critical thinking skills, and a delusionary view of the world have left the majority of Americans broke and in debt.

The data that captured my attention was how little the average American household has in savings. Roughly 62% of Americans have less than $1,000 in savings and 21% don’t even have a savings account, according to a new survey of more than 5,000 adults conducted this month by Google Consumer Survey for personal finance website GOBankingRates.com. This dreadful data is reinforced by a similar survey of 1,000 adults carried out earlier this year by personal finance site Bankrate.com, which also found that 62% of Americans have no emergency savings for a medical crisis, car repair, or unanticipated household expenditure.

In Part 1 of this article I discussed the catalyst spark which ignited this Fourth Turning and the seemingly delayed regeneracy. In Part 2 I pondered possible Grey Champion prophet generation leaders who could arise during the regeneracy. In Part 3 I will focus on the economic channel of distress which is likely to be the primary driving force in the next phase of this Crisis.

There are very few people left on this earth who lived through the last Fourth Turning (1929 – 1946). The passing of older generations is a key component in the recurring cycles which propel the world through the seemingly chaotic episodes that paint portraits on the canvas of history. The current alignment of generations is driving this Crisis and will continue to give impetus to the future direction of this Fourth Turning. The alignment during a Fourth Turning is always the same: Old Artists (Silent) die, Prophets (Boomers) enter elderhood, Nomads (Gen X) enter midlife, Heroes (Millennials) enter young adulthood—and a new generation of child Artists (Gen Y) is born. This is an era in which America’s institutional life is torn down and rebuilt from the ground up—always in response to a perceived threat to the nation’s very survival.

For those who understand the theory, there is the potential for impatience and anticipating dire circumstances before the mood of the country turns in response to the 2nd or 3rd perilous incident after the initial catalyst. Neil Howe anticipates the climax of this Crisis arriving in the 2022 to 2025 time frame, with the final resolution happening between 2026 and 2029. Any acceleration in these time frames would likely be catastrophic, bloody, and possibly tragic for mankind. As presented by Strauss and Howe, this Crisis will continue to be driven by the core elements of debt, civic decay, and global disorder, with the volcanic eruption traveling along channels of distress and aggravating problems ignored, neglected, or denied for the last thirty years. Let’s examine the channels of distress which will surely sway the direction of this Crisis.

Channels of Distress

“In retrospect, the spark might seem as ominous as a financial crash, as ordinary as a national election, or as trivial as a Tea Party. The catalyst will unfold according to a basic Crisis dynamic that underlies all of these scenarios: An initial spark will trigger a chain reaction of unyielding responses and further emergencies. The core elements of these scenarios (debt, civic decay, global disorder) will matter more than the details, which the catalyst will juxtapose and connect in some unknowable way. If foreign societies are also entering a Fourth Turning, this could accelerate the chain reaction. At home and abroad, these events will reflect the tearing of the civic fabric at points of extreme vulnerability – problem areas where America will have neglected, denied, or delayed needed action.” – The Fourth Turning – Strauss & Howe

As usual, the mainstream media reporter buries the lead in the body of the story. There is much scorn for the millennial generation by the older generations. Of course millennials will have the lowest credit scores. They have lower paying jobs and less time to build up a credit history. Duh.

The chart below actually shows Generation X to be in the worst shape. Millennials have a debt to income level of 1.5, while Gen X has a debt to income level of 2.5. Even Boomers have a debt to income level of 1.9.

Millennials are burdened with more student loan and auto loan debt than Gen X at similar ages. The eye opener is how few millennials are using credit cards – far less than Gen X at the same age. This fact combined with the fact that millennials have just surpassed the dying off Boomers as the largest generational cohort in the country, explains why retail sales have gone stagnant and credit card debt is billions lower than it was in 2008.

The millennials may have their issues, but not going into credit card debt as the political and financial status quo desires could be a game changer. An ever expanding level of consumer debt is the only thing sustaining this Ponzi Scheme. If the millennials refuse to cooperate, the game is over.

This generation of Americans has the lowest credit score

Michael D Brown / Shutterstock.com

The largest generation of Americans has the lowest credit scores.

Millennials — those roughly defined as aged between 19 and 34 — have the lowest credit scores of any generation of Americans. They have an average credit score of 625 on an average debt of $52,120. By comparison, Generation X (aged 35 to 49) have a credit score of 650 on average debt of $125,000, while both baby boomers and the Greatest Generation (with a combined age of between 50 and 87) have credit scores of 709 on average debt of $87,438.

“It’s important to keep in mind that credit scores are built on credit experiences,” says Michele Raneri, vice president of analytics and business development at Experian, while talking about millennials. “While this generation has been slower to use credit, they have plenty of opportunities to build a positive credit history.”

As usual, the MSM just flashes a headline that says consumer spending increased by 5.7% in May. Of course this is four months in a row of lower increases. That always happens during an economic recovery. Right?

The MSM bury the most important part of the report at the bottom of their regurgitated press release. Credit card debt barely inched up, by a pitiful 2.1%. Credit card debt started the year at $890 billion and five months later sits at $901 billion. That’s a 1.2% increase over five months. They tell us that the economy is fully recovered. There are 18 million more working age Americans than there were in 2008, but the amount of credit card debt outstanding is DOWN $120 BILLION!!! We are supposedly six years into a recovery with a 5.3% unemployment rate and credit card debt is down 12% from 2008.

Consumers spend more on credit when they are confident about the future and have good paying jobs. I thought consumer confidence was at seven year highs and jobs were plentiful. Obama told me so. If things are so fucking great for consumers, why is their wallet closed? Because the economic recovery storyline is a lie. Capital One commercials are on TV every 15 minutes asking the question: What’s in your wallet? The answer from John Q. Public is: NOTHING

The surge in consumer credit was again in student loans and subprime auto loans to deadbeats. The $1.4 trillion of student loans, up from $900 billion in 2010, continues to rise exponentially as the Federal government has no intention of getting repaid. You are on the hook. There are millions of low IQ Americans matriculating into the University of Phoenix, ITT and dozens of other scam schools with your money.

The government knows these schools are phony. The schools know they are phony. And most of the morons in the schools know they are phony. And you will get the bill when the defaults and bankruptcies avalanche down the mountain. But for now, the Feds give the appearance of growth.

The auto loan bubble is approaching the pin at 85 mph. The subprime slime is going bad at rates last seen in 2008/2009. The dealers lots are overflowing with inventory. The proliferation of 7 year 0% loans has reached a peak. Everyone who wanted a new car has one. The millions upon millions of leased cars are starting to hit the lots. Losses abound. The automakers profits are plummeting. The bad debt is going to destroy finance company and bank profits.

This shitshow is about to turn into a clusterfuck.

It seems hard to believe, but your government is purposely recreating the mortgage debacle of 2007 and putting you on the hook for the billions in losses coming down the road. In their frantic effort to generate the appearance of economic recovery they are willing to gamble with taxpayer’s money while luring unsuspecting blue collar folks into buying houses they can’t afford. During the previous housing bubble, greedy Wall Street bankers, deceitful mortgage brokers, and corrupt rating agencies colluded to commit the greatest control fraud in the history of mankind. This time it is your government, aided and abetted by the Federal Reserve, that is actively promoting the lending of money to people incapable of paying it back. And again, you the taxpayer will be on the hook when it predictably blows up.

The FHA, created during the first Great Depression, is supposed to be self-sustaining through mortgage insurance premiums charged to homeowners, just like Fannie, Freddie, Medicare, Social Security, and student loan lending were supposed to be self- sustaining through taxes, fees, and interest. This agency was supposed to promote homeownership for lower income Americans, but has been used by politicians as a tool to capture votes, payoff crony capitalist benefactors, and as a Keynesian stimulus tool designed to kindle a fake housing recovery. They entered the fray at the tail end of the last Fed/Wall Street created housing bubble, insuring a huge number of subprime mortgage loans from 2007 through 2009. The taxpayer has already had to bail out this incompetent, politically motivated, joke of an agency to the tune of $1.7 billion in 2014.

Edward J. Pinto, a former Fannie Mae official, estimates that under standard accounting practices the agency is already insolvent to the tune of $25 billion. Mark to fantasy accounting hasn’t just benefitted the criminal Wall Street cabal, but also the bloated pig government housing agencies – Fannie, Freddie and the FHA. The FHA’s share of new loans with mortgage insurance stood at 16.4% in 2005 and currently stands at 44.3%. This is a ridiculously high level considering the percentage of first time home buyers is near all-time lows and low income buyers have lower real median household income than they had in 2005. Distinguished congresswoman Maxine Waters, who once declared: “We do not have a crisis at Freddie Mac, and particularly Fannie Mae, under the outstanding leadership of Frank Raines.”, prior to them imploding and costing taxpayers $187 billion in losses, thinks the FHA is doing a bang up job. Her financial acumen is unquestioned, so you can expect another bailout in the near future.